You’ve heard about Dhani Loan Pay. Maybe a friend mentioned it, maybe you saw an ad, or maybe you’re already using it, and something just doesn’t feel right.

Either way, you’re here because you want to know how this thing actually works, before it affects your money or your credit score.

And that’s a smart place to start.

Because digital lending moves fast. Loan credited in minutes. EMIs auto-debited without a second prompt.

Late fees are applied before you even notice. And your credit bureau profile is updated based on whatever the lender reports, right or wrong.

At that speed, small gaps in understanding can quietly turn into bigger financial headaches.

So instead of reacting to a notification, it makes sense to slow down and understand how the Dhani loan payment system actually works.

How does the disbursal happen? How are EMIs structured? What happens if a payment is reflected as late? And more importantly, is it safe to proceed?

In this Dhani loan pay review, we’ll examine the payment process, the company’s regulatory status, RBI action taken in the past, public news reports, and user-reported payment issues- all in one structured analysis.

Let’s begin with how the Dhani loan pay actually works.

Dhani Loan Pay Review

Dhani Loan Pay is a fully digital loan and repayment system that lets you borrow money, manage EMIs, and track dues, all from your phone, without stepping into a bank.

After approval and digital KYC, the loan amount is credited directly to your registered bank account.

Repayment dates are fixed in advance, and EMIs are typically deducted through an auto-debit mandate.

Processing fees and other charges are applied as per the loan terms shared at the time of sanction.

Most concerns arise during repayment. If there isn’t enough balance on the due date, the EMI can fail and attract bounce charges.

If a payment is made close to the reporting cycle, it may still reflect as overdue for that period.

Since lenders report repayment behaviour to credit bureaus in scheduled intervals, even short delays can affect the credit profile.

Because everything runs through automated systems, even small timing differences can create confusion.

Reviewing the detailed loan statement, including the breakup of principal, interest, and charges, usually provides more clarity than relying on app notifications alone.

To identify whether a concern is technical, timing-related, or more serious, it is helpful to first understand how Dhani Loan Pay functions from disbursal to EMI repayment.

How Dhani Loan Pay Works?

Before you question the payment, understand the structure behind it. Dhani Loans & Services Limited operates as a digital NBFC.

The entire process from approval to repayment happens inside the app.

Once you apply and complete digital KYC using your Aadhaar and PAN, the system evaluates your profile and generates a loan offer.

If you accept the offer, the loan amount gets credited directly to your bank account.

Now here’s something many borrowers overlook.

The amount credited may not always match the headline loan amount shown on the screen.

Lenders usually deduct processing fees, convenience charges, or other applicable costs before disbursal.

The sanction letter clearly mentions these details, but most people don’t read it carefully. That’s where confusion begins.

When it comes to repayment, the Dhani loan pay works through structured EMIs.

The app typically sets up an auto-debit mandate (NACH). On the due date, the EMI gets deducted automatically from your linked bank account.

If the debit fails due to insufficient balance, the system may apply bounce charges and mark the payment as overdue. And this is important.

Even a small overdue amount can reflect in credit bureau reporting.

Lenders update repayment behaviour to credit bureaus like CIBIL. A delay, even of a few days, can affect your credit profile depending on reporting cycles.

So technically, the Dhani loan pay system is automated and rule-based.

It credits the loan digitally. It deducts EMIs automatically. It reports repayment behaviour to credit bureaus.

Now comes the bigger question. Is the system structured and digital?

Let’s examine that using regulatory records, not opinions.

Is Dhani Loan Pay Legit?

If you are trying to figure out whether Dhani loan pay is genuine, the first thing to check is its regulatory status.

Dhani Loans & Services Limited is registered with the Reserve Bank of India (RBI) as a Non-Banking Financial Company (NBFC).

That means it operates under RBI regulation and supervision.

It is not an unregistered or anonymous loan application functioning outside the financial system.

This directly addresses the common concern people have when they wonder, “Dhani Loan Pay Real or Fake?”

From a registration standpoint, the company is legally recognized.

However, registration alone does not mean there has been no scrutiny.

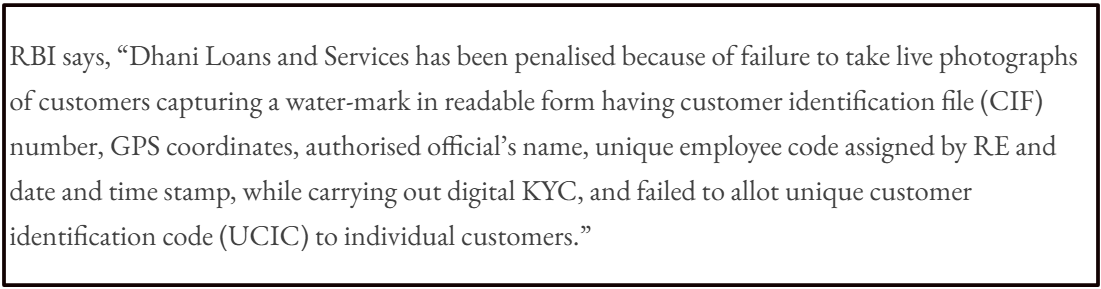

During supervisory inspections, RBI reviewed Dhani’s digital onboarding and compliance processes and identified certain deficiencies related to digital KYC procedures.

Here is what RBI observed.

RBI noted gaps in the digital KYC process, including issues related to live photograph capture and adherence to prescribed identification standards.

Digital KYC is critical because it verifies borrower identity during loan approval.

Following these findings, RBI imposed a monetary penalty.

RBI imposed a monetary penalty of Rs. 20 Lakh on Dhani Loans & Services Limited for non-compliance with specific regulatory directions. Importantly, the regulator did not cancel the NBFC registration.

The action focused on correcting procedural lapses rather than declaring the platform illegal. So what does this mean in practical terms?

Dhani loan pay operates under a valid RBI registration.

At the same time, it has faced regulatory action for compliance deficiencies. That combination reflects regulatory oversight, not invisibility, and not immunity.

Legitimate from a registration perspective. Subject to scrutiny from a compliance perspective.

Understanding that distinction helps separate legal status from public debate.

Is Dhani Loan Pay Safe?

Now that we’ve looked at its regulatory position, the more practical concern is whether Dhani Loan Pay is actually safe to use.

Safety in digital lending depends on multiple factors.

Registration under RBI provides regulatory oversight, but user experience, verification systems, and fraud risks in the wider ecosystem also play an important role.

To understand this better, we need to look at two key areas that have shaped public concern.

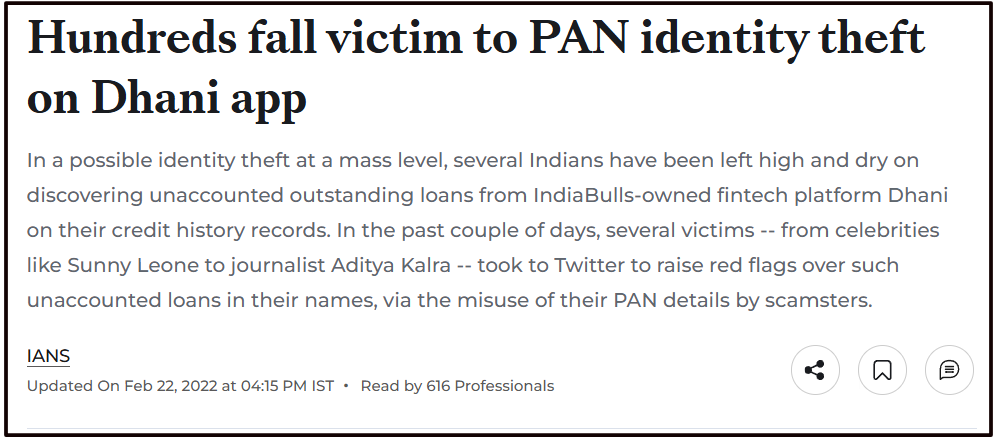

1. Identity Misuse

Over the past few years, media reports have discussed cases where individuals claimed that loan entries appeared against their PAN without their clear knowledge.

These reports raised questions about digital onboarding processes and document verification standards.

Reports like this create understandable concern.

If a person sees a loan entry linked to their PAN without having knowingly taken a loan, it immediately raises questions about verification controls.

However, such reports highlight alleged identity misuse or verification gaps.

They do not automatically amount to a legal declaration that the platform itself is fake.

In digital lending, compromised documents or weak verification processes can sometimes lead to unauthorised entries in credit records.

This becomes a compliance and data security issue, which regulators monitor through inspections and corrective action.

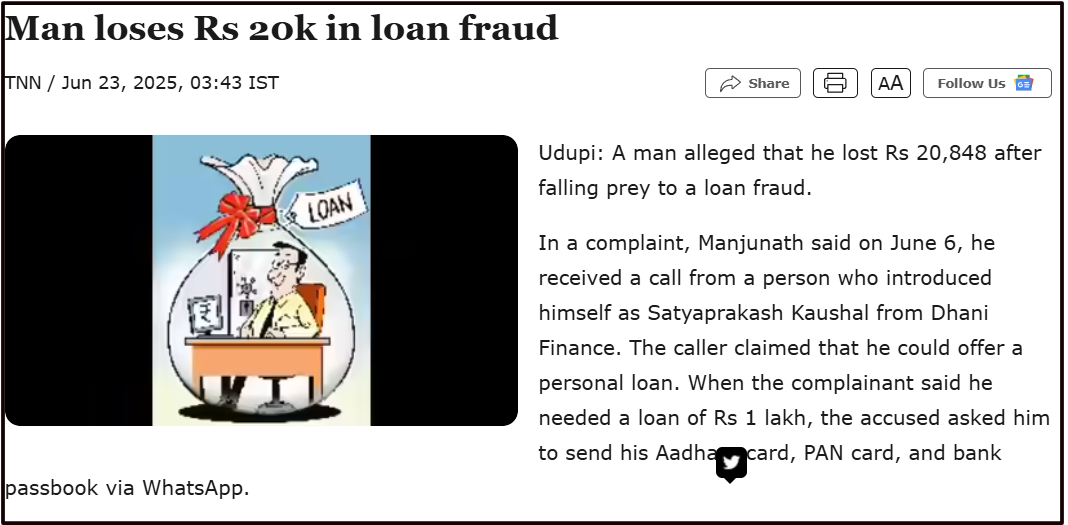

2. Impersonation Fraud

Another important aspect is impersonation fraud.

There have been instances in the digital lending ecosystem where fraudsters posed as representatives of loan companies and demanded advance payments or insurance fees.

In such cases, individuals were asked to transfer money to personal UPI IDs or unrelated bank accounts. After payment, the fraudsters stopped responding.

These incidents involve criminal misuse of brand names rather than official in-app loan transactions.

For regulated NBFCs, repayment is structured through predefined EMI systems within the platform or authorised payment channels.

Requests for direct transfers to personal accounts, especially through phone calls or WhatsApp messages, should always be verified carefully.

From a regulatory standpoint, it operates under RBI registration.

3. Data Privacy Concerns

Digital loan apps typically request access to contacts, location, and device data during onboarding, and how that data is stored or used isn’t always transparent to the borrower.

Several users across lending platforms have raised concerns about receiving unsolicited calls or messages, suggesting data may have been shared beyond what was expected.

While this isn’t unique to Dhani Loan Pay, it’s worth being aware of what permissions you’re granting when you sign up. Always review the app’s privacy policy before completing registration.

If something feels excessive, that’s worth questioning before you proceed.

At the same time, the broader digital lending ecosystem has seen cases of identity misuse, impersonation fraud and data privacy gaps.

This means safety depends not only on the platform’s status but also on how borrowers verify communications and handle payments.

Now, let’s examine what users themselves report about Dhani loan payment issues and how those complaints influence perception.

Dhani Loan User Complaints

Even when a loan system runs digitally and automatically, repayment disputes can still happen. And when money is involved, even a small mismatch feels bigger than it is.

If you go through online reviews related to Dhani loan pay, you’ll notice something interesting.

Most complaints don’t question loan approval. They question repayment clarity, especially outstanding balances and the impact on credit score.

Let’s examine what users are saying, and more importantly, what those complaints could mean.

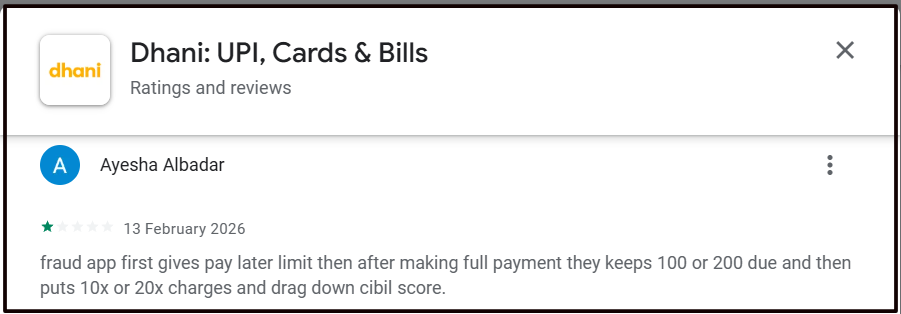

1. Outstanding Balance Showing Even After Payment

Several users online claim that they cleared their dues, yet the app continued to show an outstanding amount.

For a borrower, that immediately raises concern, especially when reminders or calls follow.

Here’s one such review:

The user alleges that despite making a full payment, the system continued to reflect dues.

Situations like this usually create anxiety because borrowers worry about late fees or CIBIL damage.

Now let’s slow this down.

In digital lending, paying an EMI and closing a loan are not always the same event.

Interest accrues daily. If a payment reflects slightly after the billing cut-off, a small balance may remain.

Bounce charges can also apply if auto-debit fails even once. Sometimes payment posting delays create temporary discrepancies.

That doesn’t automatically validate or dismiss the complaint.

It simply means borrowers should always download the detailed loan statement and verify final settlement amounts instead of relying only on the EMI screen.

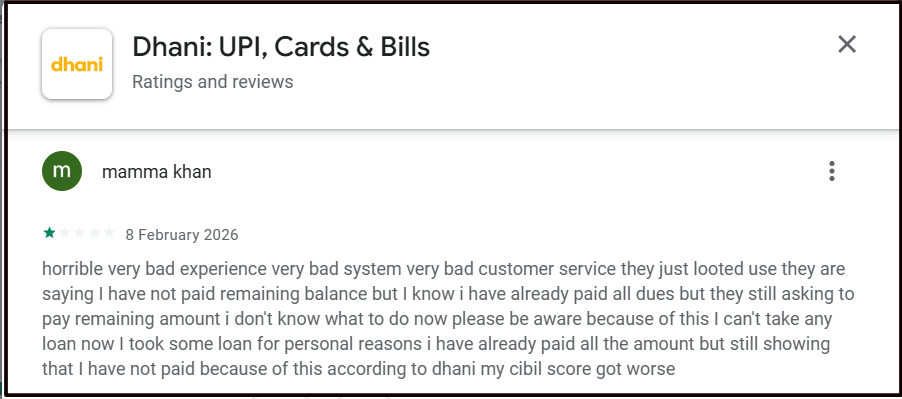

2. CIBIL Score Impact After Payment

Another theme that appears repeatedly in reviews relates to credit score impact.

Some users allege that even after paying their dues, their CIBIL score dropped or showed a delayed payment status. Take a look at this example.

When a lender reports repayment behaviour to credit bureaus, it follows a reporting cycle.

If the system marks a payment as overdue on the reporting date, even briefly, the bureau may update that status. Once reported, the credit score adjusts accordingly.

If a borrower believes the reporting is incorrect, they can raise a formal dispute with the credit bureau. The bureau then contacts the lender for clarification.

So the key takeaway here is this: repayment timing, reporting cycles, and small dues can affect credit records more quickly than borrowers expect.

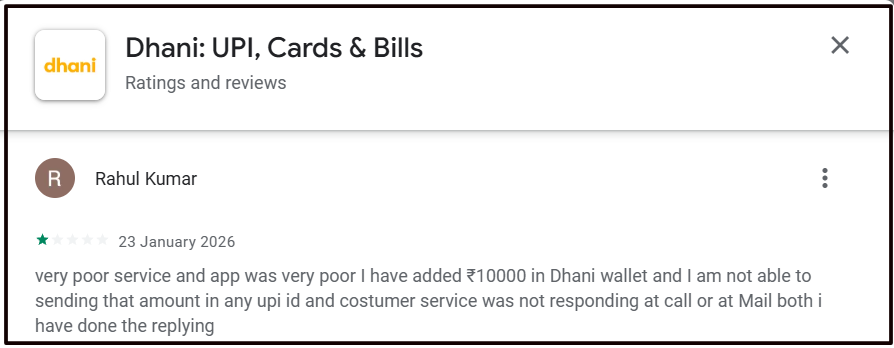

3. Wallet and Transfer Issues

Apart from EMI disputes, some users also report operational concerns related to wallet balances and transfers.

Here is one such example.

In this case, the user claims difficulty transferring funds and receiving support.

Now, it’s important to distinguish between the two services. A wallet function and a loan repayment system operate differently, even if they exist inside the same app.

A wallet issue does not automatically affect the legality of the loan agreement, but it can affect customer confidence and overall experience.

Service responsiveness plays a major role in how safe borrowers feel, especially when money is involved. By now, you’ve seen both sides:

The structured repayment system on paper and the disputes some users raise online. So if something feels unclear or incorrect in your own case, what should you actually do?

Let’s talk about the correct way to report a loan app scams.

How to Complain Against the Loan App?

When a payment dispute happens, don’t panic and don’t ignore it. Follow a structured approach.

The faster you act, the easier it is to fix.

1. Contact the Official Customer Support First

Start with the lender itself.

Dhani Loans & Services Limited, as an RBI-regulated NBFC, must maintain a grievance redressal system.

Raise your complaint through the official app, email, or registered customer support channel.

Ask for:

- A detailed statement of account.

- Breakup of principal, interest, and charges.

- Confirmation of payment posting.

Keep written proof of every communication. Avoid relying only on verbal assurances over phone calls.

2. Raise a Credit Bureau Dispute if CIBIL is Affected

If your CIBIL score dropped after a payment dispute, you don’t have to wait.

You can raise a dispute directly with the credit bureau (such as CIBIL) through their online portal. Once you submit the request, the bureau contacts the lender for clarification.

If the reporting was incorrect, they will update your credit record.

Always check your credit report after clearing dues to ensure it reflects correctly.

3. File Cybercrime Complaint

If someone asks you to transfer money outside the official app, especially through personal UPI IDs or bank accounts, stop immediately. That is a red flag.

In such cases:

- Do not send money.

- Inform the official loan app.

- File a complaint on the National Cyber Crime Reporting Portal.

- Keep call logs and screenshots as evidence.

Impersonation fraud is common in digital lending. Official EMI payments happen inside the regulated system, not through random calls.

4. Escalate the Complaint to RBI if Unresolved

If the lender does not resolve your complaint within a reasonable time, you can escalate it through the RBI Complaint Management System (CMS).

RBI allows customers to file complaints against regulated NBFCs if internal grievance redressal fails. This adds regulatory oversight to your issue.

Always escalate in steps, lender first, regulator next.

5. Document Everything Before Making a Payment

Before you clear any outstanding amount:

- Download the latest loan statement

- Confirm the exact payable amount

- Keep proof of transaction

- Take screenshots of successful payment

Documentation protects you if a dispute arises later.

This structured approach ensures that you act logically, not emotionally.

Need Help?

If you’re dealing with an unresolved Dhani Loan Pay issue, whether it’s an incorrect outstanding balance, a credit score dispute, or confusing repayment charges, you don’t have to figure it out alone.

Check out the details in our online loan response plan for step-by-step guidance on how to file your complaint the right way and get it resolved faster.

Conclusion

When you search for a Dhani loan pay review, you’re not just looking for information; you’re looking for clarity before making a financial decision.

Dhani Loans & Services Limited operates as an RBI-registered NBFC. The loan disbursal and repayment system runs digitally through structured EMIs and automated reporting to credit bureaus.

At the same time, RBI has imposed monetary penalties in the past for compliance lapses related to digital KYC procedures. Public news reports and online reviews also show that some borrowers have raised concerns about repayment disputes and credit score impact.

That doesn’t automatically make the platform fake. It also doesn’t mean every complaint lacks merit.

It simply means this: digital loan payments require awareness.

Before making any Dhani loan payment, verify your outstanding amount, review your loan statement, and ensure you use only official payment channels. If something doesn’t add up, address it early and escalate through the proper route.

Clarity protects your money. Documentation protects your credit.