You don’t search “Dhani loan real or fake” unless something feels off.

Maybe you received an unexpected payment reminder.

Maybe an outstanding amount still shows after you paid, your CIBIL score changed, or online reviews made you question whether the platform itself is genuine.

In the world of digital lending, confusion spreads quickly. A few complaints, a news report, and suddenly the bigger question arises: Is Dhani loan real, or is something wrong?

Before assuming anything, it’s better to look at the facts.

Let’s examine its registration status, RBI action, public reports, and user complaints and then answer the question clearly.

Dhani Loan Review

Dhani Loan sits at the intersection of convenience and doubt.

On one hand, it offers quick digital loans and app-based repayment. On the other hand, online searches show people questioning its legitimacy, discussing RBI action, and sharing mixed experiences.

That contrast creates uncertainty.

When you receive an EMI reminder, see an outstanding amount that doesn’t make sense, or notice a change in your credit score, your mind doesn’t immediately think about reporting cycles or compliance procedures.

It jumps to a bigger question: is something wrong with this platform?

But confusion doesn’t always mean fraud. Sometimes it reflects regulatory scrutiny. Sometimes it reflects user disputes.

And sometimes it reflects impersonation scams that misuse brand names.

To understand what’s really happening, we need to examine the platform’s legal standing and regulatory history first.

Let’s address the core question directly: Is the Dhani loan real or fake?

Is Dhani Loan Real or Fake in India?

Let’s address the question clearly.

Dhani Loans & Services Limited operates as a Non-Banking Financial Company (NBFC) registered with the Reserve Bank of India.

RBI grants this registration and regulates its operations. This means Dhani does not function as an anonymous or unregulated loan app.

From a registration standpoint, Dhani loan is a legally recognised financial entity.

However, registration does not place a company beyond regulatory review.

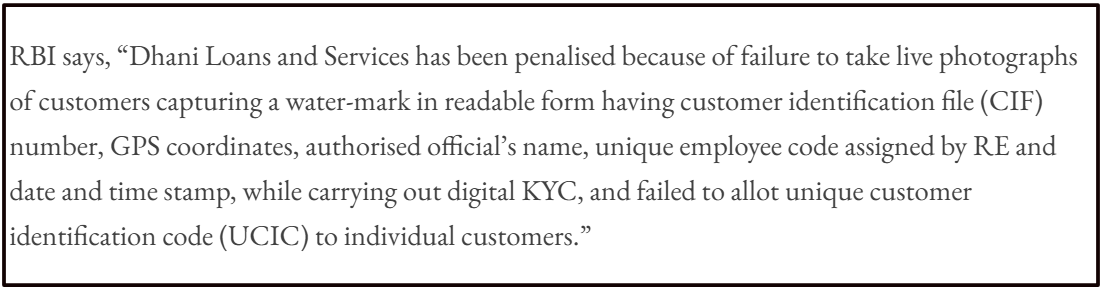

RBI conducted supervisory inspections and examined Dhani’s compliance framework, particularly its digital KYC procedures.

During this inspection, RBI identified deficiencies in how the company implemented certain onboarding requirements.

As shown above, RBI pointed out gaps related to digital KYC compliance standards.

Digital KYC verifies borrower identity during loan approval. When RBI identifies weaknesses in this process, it signals compliance issues that require correction.

This distinction is important.

A compliance lapse does not make a platform fake. It shows that the regulator is actively monitoring and enforcing standards.

So if the question is whether the Dhani loan exists as a real financial entity, the answer is yes. It operates under RBI registration and regulatory supervision.

Now let’s examine what that registration actually means and what it does not guarantee.

Is Dhani Loan Registered?

Yes, Dhani Loans & Services Limited holds registration as an NBFC with the Reserve Bank of India.

RBI grants NBFC registration only after a company meets prescribed financial and compliance requirements.

Once registered, the entity must follow RBI guidelines related to lending practices, KYC norms, grievance redressal, and reporting standards.

That means the Dhani loan does not operate outside the financial system. It functions under regulatory supervision.

However, registration does not mean the company has never faced regulatory action.

After conducting inspections, RBI imposed a monetary penalty on Dhani Loans & Services Limited for non-compliance with certain regulatory directions.

As reflected above, RBI imposed a ₹20 lakh penalty for compliance lapses. Importantly, RBI did not cancel the company’s NBFC registration. The regulator chose to penalise and correct, not shut down operations.

This distinction matters when evaluating whether a platform is real or fake.

Fake loan apps operate without registration and outside RBI oversight. In this case, RBI regulates the entity, conducts inspections, and enforces compliance through penalties where necessary.

Registration confirms legal existence. Regulatory penalties confirm oversight.

Now that we’ve clarified the registration status, let’s look at the media coverage that has shaped public perception.

Dhani Loan Safe or Not

When people question whether the Dhani loan is safe or a scam, media coverage often plays a big role in shaping that doubt.

News headlines carry weight. A single article can influence public perception more than dozens of user reviews.

Instead of reacting emotionally to rumours, let’s examine the specific patterns reported by news outlets and regulatory bodies to separate operational growing pains from the broader threat of loan app scams.

1. PAN Identity Misuse Reports

Some media reports highlighted cases where individuals allegedly found loan entries linked to their PAN details without clear knowledge or consent.

As seen above, the report discusses concerns around identity verification and digital onboarding practices.

When someone notices an unfamiliar loan entry in their credit report, the first reaction is suspicion.

That suspicion often expands into a broader question about whether the platform itself is genuine.

Identity misuse can occur due to data compromise, weak verification controls, or fraudulent third-party activity, and regulators usually step in to review such lapses.

The key point here is this: a report about misuse does not automatically mean the company itself is fake. It indicates scrutiny and concern.

2. Fraud and Impersonation Cases

Separate from onboarding concerns, law enforcement authorities have also taken action in cases where fraudsters allegedly used the names of digital loan platforms to deceive borrowers.

In these cases, individuals reportedly posed as representatives, demanded advance insurance fees, or asked for payments outside official app channels.

After receiving money, they disappeared. This is a classic impersonation pattern.

Fraudsters often misuse brand names to appear legitimate. They contact victims through phone calls or messaging apps and request urgent payments.

These activities happen outside regulated systems.

Understanding this distinction matters when evaluating whether the Dhani loan is safe or not.

A registered NBFC operates within RBI oversight and structured payment systems. Impersonators operate outside those boundaries.

Now, let’s look at what actual users have alleged about the Dhani Loan.

Dhani Loan User Complaints

Online reviews heavily influence how people judge whether a loan app is real or fake. When repayment issues appear, doubt grows quickly.

Let’s look at the types of complaints users have raised.

1. Outstanding Dues After Payment

Some users allege that even after clearing their loan amount, the app continued to show an outstanding balance.

In situations like this, frustration builds immediately. If someone believes they paid in full and the system still shows “due,” they begin to question the platform’s credibility.

Loan systems calculate interest daily.

If a payment reflects after a cut-off date, or if a small charge remains unpaid, the account may not close automatically. Auto-debit failures and bounce charges can also leave residual amounts.

That explanation doesn’t dismiss the complaint, but it shows how timing and calculation mechanics can create confusion.

2. Allegations of Legal Notices and Aggressive Recovery Calls

A few reviews claim that users received legal notices or threatening calls demanding repayment.

Allegations of aggressive recovery communication raise serious concerns. Words like “legal action” or “police visit” create fear quickly.

However, digital lending also faces impersonation scams. Fraudsters sometimes pose as recovery agents and pressure individuals into making payments.

Without verified investigation findings, these remain user allegations, not proven conclusions.

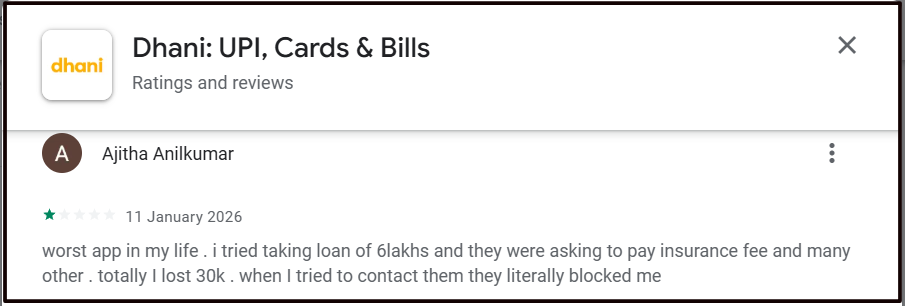

3. Allegations of Upfront Insurance or Processing Fee Demands

Some users allege that representatives asked them to pay insurance fees or other charges separately before disbursal, after which communication stopped.

Advance fee demands often raise red flags. Regulated lenders typically deduct processing charges from the sanctioned amount rather than requesting separate transfers to personal accounts.

When someone requests payment outside official app channels, caution becomes necessary.

Whether such cases reflect internal misconduct or impersonation requires investigation, but from a borrower’s perspective, the risk feels real.

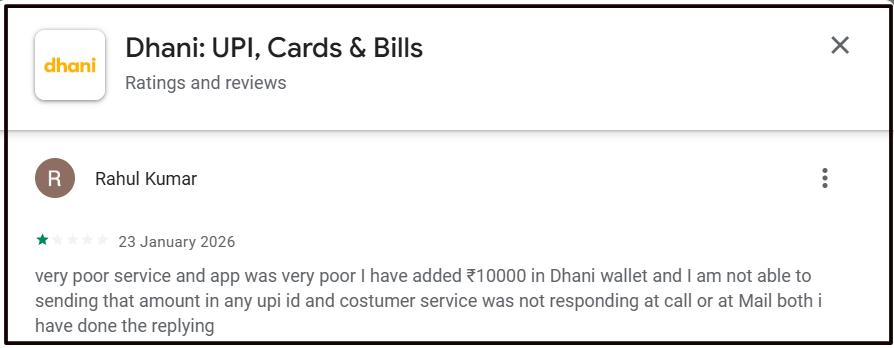

4. Complaints About Wallet and Customer Support Issues

Some reviews mention difficulty transferring wallet balances or receiving timely responses from customer support.

Service issues do not automatically define whether a platform is fake. However, poor communication can increase distrust, especially when money is involved.

Service issues, repayment disputes, aggressive call allegations, advance fee claims, these are serious concerns when you read them one after another.

But when you face a situation like this, the real question becomes practical:

What should you actually do if you believe something is wrong?

Instead of debating online, it’s better to follow a structured route. Let’s look at how you can report a loan app issue properly and protect yourself.

How to Complain Against the Loan App?

If something feels wrong, an unexplained large amount, a credit score drop, or a suspicious payment demand, don’t ignore it and don’t panic. Follow a structured approach.

1. Contact the Lender First

Start with the official source.

Raise a written complaint through the Dhani app or its registered customer support email.

Ask for a detailed statement of account. Request a clear breakup of principal, interest, late fees, and any additional charges.

Keep everything in writing. Save screenshots. Store payment receipts. Documentation protects you if the dispute escalates.

2. Raise a Credit Bureau Dispute (If CIBIL Is Affected)

If your credit score reflects overdue status despite payment, log in to the official credit bureau portal and file a dispute.

The bureau will contact the lender for clarification.

If the lender reported incorrect information, the bureau will update your record. Always monitor your credit report after clearing dues.

3. File a Cyber Crime Complaint

Report the incident on the National Cyber Crime Reporting Portal and notify the official loan app through its verified customer support channels so they are aware of the misuse.

Remember, fraudsters often create urgency to pressure you into quick decisions. Genuine lenders process repayments only through their official platforms.

Never through personal accounts or informal payment links.

4. Escalate to RBI if the Issue Remains Unresolved

If the lender fails to resolve your complaint within a reasonable time, you can escalate the matter through the RBI Complaint Management System (CMS).

RBI allows customers to file complaints against regulated NBFCs when internal grievance mechanisms fail. This adds regulatory oversight to your case.

Follow the process step by step. Stay calm. Act formally.

Now, if you feel unsure about handling the dispute on your own, here’s how we can help.

Need Help?

Loan disputes can feel overwhelming, especially when they involve outstanding dues, credit score impact, or threatening communication.

If you are facing unresolved issues related to the Dhani loan and you’re unsure how to proceed, we can assist.

When you register with us, our team reviews your loan agreement, repayment history, and credit report carefully.

We examine whether the charges applied match the sanctioned terms and whether the credit reporting reflects your actual payment status.

If required, we guide you through the proper escalation process.

That may include drafting structured complaints, responding to recovery communication, or approaching the appropriate regulatory authority.

Conclusion

Dhani Loans & Services Limited is registered with the Reserve Bank of India as a Non-Banking Financial Company (NBFC).

That means it legally exists and operates under RBI supervision.

In fact, the RBI has imposed monetary penalties on the company in the past for compliance lapses, which shows that regulatory oversight is active.

At the same time, there have been media reports raising concerns about alleged identity misuse.

Online reviews mention repayment disputes, credit bureau reporting issues, and customer service complaints.

Adding to the confusion, fraudsters have also misused the Dhani brand name in impersonation scams.

So what does all this actually mean? So, is Dhani Loan real or fake?

Registration confirms legal existence. Regulatory penalties confirm supervision. Customer complaints reflect dissatisfaction. But none of these factors alone tells the complete story.

If you are dealing with Dhani Loan, the smartest approach is caution, not assumptions. Verify every loan detail carefully.

Use only official apps, websites, and customer care numbers. Keep records of agreements, payments, and communications. And if a dispute arises, escalate it through formal grievance and regulatory channels.

In financial matters, clarity and documentation protect you far more than opinions ever will.