Before taking any digital loan, safety matters more than speed.

Dhani Loan Pay offers quick approvals and app-based access, which makes borrowing feel simple.

But convenience alone doesn’t remove risk. In digital lending, even a small issue, a delayed EMI, an unexpected charge, or a reporting mismatch, can affect your credit score and create unnecessary stress.

You may have seen mixed reviews online. You may have read about regulatory action or fraud cases in the news. That naturally raises concern.

Instead of relying on opinions, it’s better to examine the facts. Is Dhani loan registered? Has it faced regulatory scrutiny? What risks should borrowers actually watch before taking or repaying a loan?

Let’s assess whether the Dhani loan is safe, based on registration, regulatory action, public reports, and real user complaints.

Is Dhani Loan Registered?

Let’s start with the basic foundation, which is registration.

Dhani Loans & Services Limited operates as a Non-Banking Financial Company (NBFC) registered with the Reserve Bank of India (RBI).

RBI regulates NBFCs and sets rules around lending practices, KYC norms, grievance redressal, and reporting standards.

This means Dhani does not operate as an unregistered or anonymous loan app. It functions within India’s regulated financial framework.

However, being “registered” is the bare minimum requirement; it is not a seal of perfection.

While registration answers the technical question of whether the Dhani loan is real or fake, it doesn’t necessarily account for the user experience.

RBI registration ensures the company exists legally, but it does not prevent:

- Technical Glitches: System errors that might show incorrect outstanding balances.

- Customer Service Gaps: Delays in resolving disputes or closing accounts.

- Aggressive Recovery: Instances where third-party recovery agents might overstep, leading to regulatory warnings.

In fact, the RBI has a history of penalising even the largest NBFCs when they find gaps in “digital lending” practices or debt recovery methods.

Therefore, the existence of an RBI license proves the app is real, but it doesn’t exempt the user from due diligence regarding hidden charges or credit score reporting errors.

The next step is more important as it is also necessary to know whether the services are safe or not.

Is Dhani Loan Safe in India?

Registration answers only one part of the question. Safety goes beyond legality. It includes how a company follows compliance rules, how it handles customer data, and how it responds to borrower concerns.

Let’s look at the risk factors one by one.

1. RBI Action and Compliance Gaps

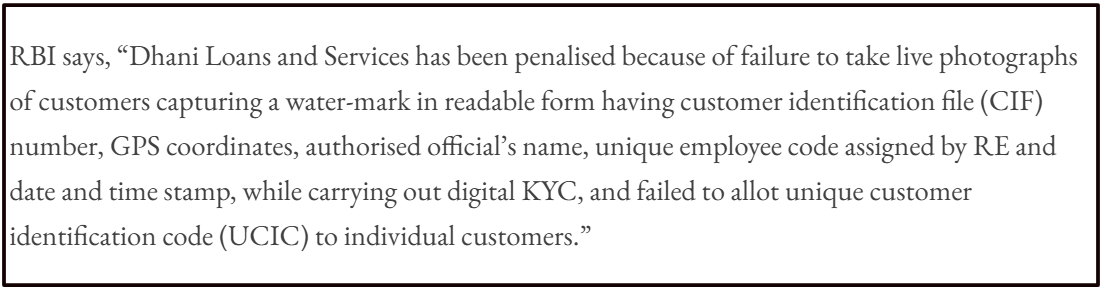

RBI conducted inspections of Dhani Loans & Services Limited and examined its digital KYC processes.

During this review, the regulator identified deficiencies in how certain onboarding requirements were implemented.

Digital KYC verifies borrower identity during loan approval. When RBI flags gaps in this process, it signals compliance concerns that require correction.

RBI did not stop at observation. It imposed a monetary penalty on the company for non-compliance with regulatory directions.

The regulator imposed a ₹20 lakh penalty. However, RBI did not cancel the NBFC registration. The company continues to operate under supervision.

What does this mean for safety?

It shows that RBI actively monitors the entity and takes corrective action when necessary. At the same time, it confirms that the company has faced regulatory scrutiny.

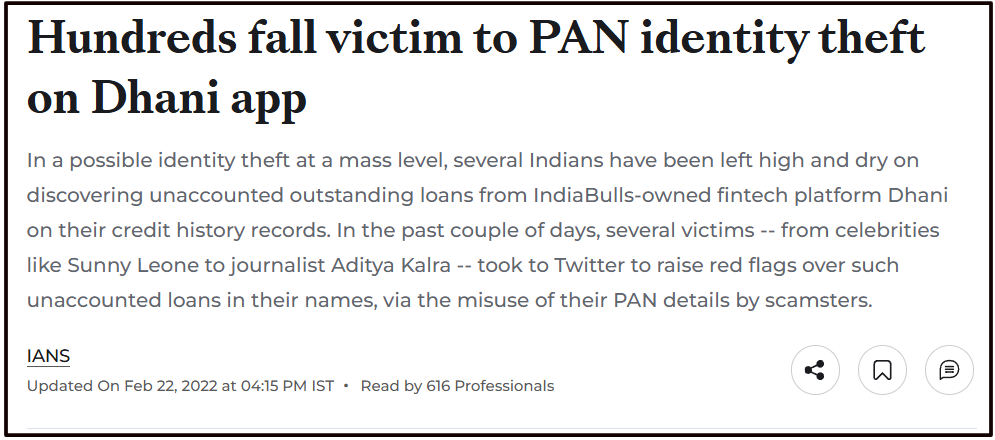

2. Media Reports on Identity Misuse

Public safety perception also depends on media coverage. Some reports have highlighted cases where individuals allegedly found loan entries linked to their PAN details without clear consent.

Reports like these raise concerns about data protection and verification controls. When borrowers see unexpected entries in their credit history, they naturally question the platform’s safety.

It’s important to note that media reports describe alleged incidents. They do not automatically establish criminal findings against the company. Still, such coverage increases public caution.

3. Fraud and Impersonation Risks

Digital lending platforms often attract impersonation scams. Fraudsters sometimes use the name of legitimate companies to demand advance payments or insurance fees.

In such cases, individuals reportedly posed as representatives and requested payments outside official app channels. These schemes operate outside regulated systems but create confusion around the brand.

Advance fee demands, personal UPI transfers, and pressure-based calls are clear red flags.

So, is Dhani loan safe?

It operates as a registered NBFC under RBI supervision. At the same time, it has faced compliance scrutiny, and the broader digital lending ecosystem carries fraud risks.

Safety depends not just on the company’s status, but also on how carefully borrowers verify payments and documentation.

Now let’s look at what actual users have reported about their experiences.

Dhani Loan Complaints

Regulatory action and news reports tell one side of the story. User experiences tell another.

While Dhani is a legitimate entity registered as a Non-Banking Financial Company (NBFC), the friction users experience often mirrors the predatory tactics found in loan app scams.

These scams have become a growing plague in the digital lending space, typically following a dangerous pattern.

Let’s look at the most significant concerns users have raised.

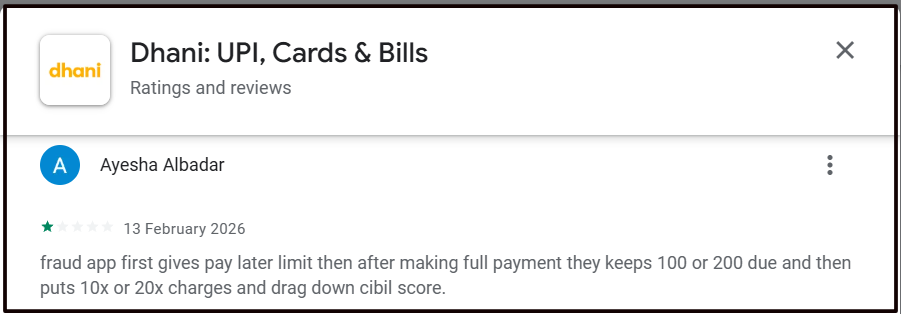

1. Outstanding Dues After Payment

Some users allege that even after clearing their loan amount, the app continued to show an outstanding balance.

When a borrower pays and still sees “due” in the app, trust drops immediately. In digital lending, interest accrues daily, and late fees apply automatically.

If a payment reflects after a reporting cut-off, even a small balance can remain.

That explanation does not dismiss the complaint. It shows how system timing can create confusion, but for the borrower, the experience feels risky.

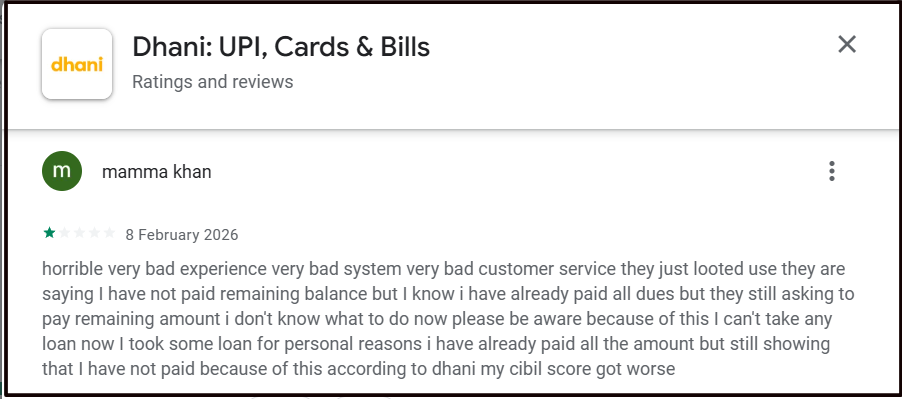

2. CIBIL Score Impact Allegations

Another common concern involves credit score changes.

Some users claim that despite making payments, their CIBIL score dropped. Lenders report account status to credit bureaus on scheduled dates.

If the system marks an account overdue at the time of reporting, the bureau records it.

Once recorded, the score reacts.

Borrowers who don’t understand reporting cycles often interpret this as unfair treatment. A credit score directly affects loan eligibility, so safety concerns increase quickly.

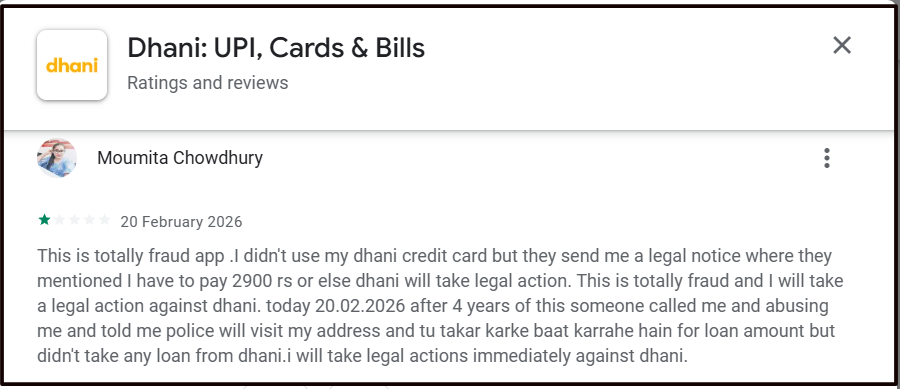

3. Legal Notice and Recovery Call Allegations

A few reviews go further. Some individuals allege that they received legal notices or threatening recovery calls demanding repayment.

Allegations of aggressive recovery communication raise serious safety concerns. At the same time, impersonation scams remain common in digital lending.

Fraudsters sometimes pose as recovery agents and create urgency to pressure payment.

Without verified findings, these remain user allegations, but they highlight why borrowers feel uneasy.

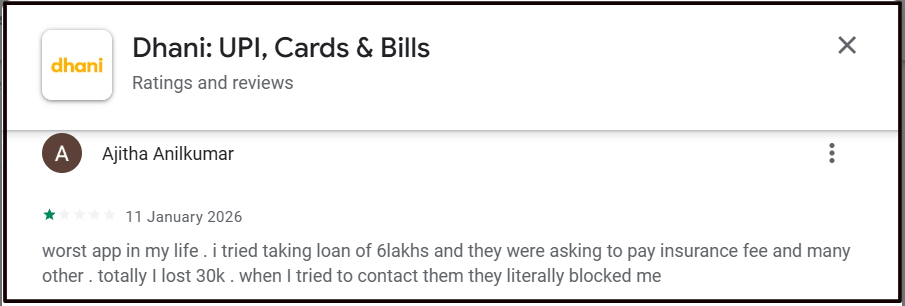

4. Upfront Insurance Fee Allegations

Some users also allege that representatives asked them to pay insurance fees or additional charges separately before disbursal.

Advance fee demands often signal risk. Regulated lenders typically deduct processing fees directly from the sanctioned amount rather than asking for separate transfers to personal accounts.

When borrowers encounter requests outside official app channels, caution becomes necessary.

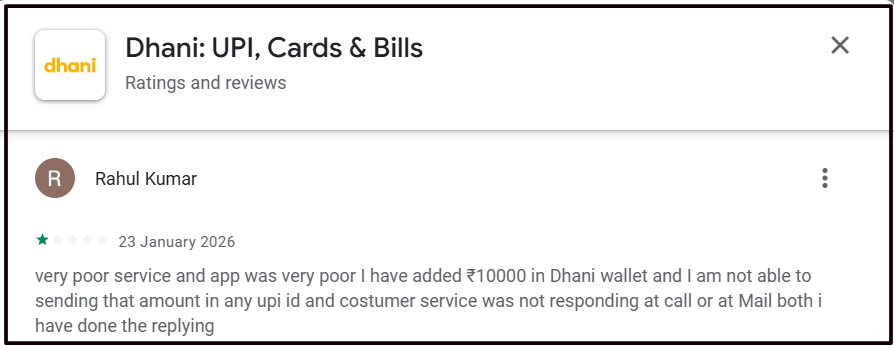

5. Wallet and Customer Support Issues

Some complaints focus on operational problems, such as difficulty transferring wallet balances or receiving timely responses from support.

Service gaps do not automatically make a company unsafe. But when support feels unresponsive, borrowers lose confidence — especially when money is involved.

These complaints reflect dissatisfaction and dispute patterns. They do not serve as judicial conclusions, but they do explain why many people question safety.

If you encounter any of these issues, the next step matters more than online debate. Let’s look at how you can report unsafe loan practices properly.

How to Complain Against the Loan App?

If you believe a loan interaction feels unsafe, whether it involves unclear dues, pressure tactics, or suspicious payment demands, take control of the situation calmly.

Follow a clear escalation path instead of reacting emotionally.

Step 1: Create a Written Record

Before escalating, organise your documents.

- Download your loan agreement.

- Save your repayment receipts.

- Take screenshots of outstanding amounts and payment confirmations.

Clear documentation strengthens your position. Verbal complaints rarely solve financial disputes.

Step 2: Contact the Official Grievance Channel

Reach out through the lender’s official grievance redressal system. Use the app, website email, or registered contact details, not numbers shared over calls or messages.

State your issue clearly. Ask for:

- A full statement of account

- Clarification of charges

- Written confirmation of your payment status

Insist on written replies.

Step 3: Protect Your Credit Report

If your credit score reflects incorrect overdue status, log in to the credit bureau’s official website and file a dispute.

The bureau will contact the lender for verification. If the reporting does not match your repayment records, they will correct it.

Monitor your credit report regularly when you close or repay a loan.

Step 4: File a Cyber Crime Complaint

If someone demands advance insurance fees, asks for payment to a personal UPI ID, or threatens police action over phone calls, treat it as a red flag.

Do not transfer money.

File a complaint on the Cyber Crime Reporting Portal. Keep call logs and screenshots as evidence.

Regulated loan repayments happen through official systems, not through urgent personal transfers.

Step 5: Escalate to RBI if Necessary

If the lender does not resolve your complaint within a reasonable period, escalate the issue through the RBI Complaint Management System (CMS).

RBI reviews complaints against regulated NBFCs when internal grievance processes fail. This step brings regulatory oversight into the matter.

When it comes to safety, speed matters less than structure.

Document first. Escalate formally. Protect your credit record.

Now, if you want structured support while handling such a dispute, here’s how we can help.

Need Help?

Loan safety concerns can escalate quickly, especially when they involve credit score impact, recovery communication, or unclear charges.

If you are facing a dispute related to a Dhani loan and you want clarity before taking the next step, we can assist.

When you register with us, we review your loan documents, repayment history, and credit report in detail.

We assess whether the charges applied match the agreement and whether the credit reporting reflects your actual payment status.

If necessary, we help you prepare structured complaints and guide you through the appropriate escalation channels.

A documented and methodical approach often prevents unnecessary financial and credit damage.

If you want to handle the situation carefully and professionally, you can register with us for guidance.

Conclusion

So, is Dhani loan safe?

Dhani Loans & Services Limited operates as an RBI-registered NBFC. That confirms legal registration and regulatory supervision.

At the same time, RBI has identified compliance lapses in the past and imposed monetary penalties.

Media reports have highlighted identity misuse concerns, and user reviews reflect repayment disputes and service complaints.

Fraud impersonation remains a broader risk in the digital lending space.

None of these factors alone defines absolute safety or absolute danger.

Dhani loan is not an unregistered or anonymous app.

But like any digital lending platform, it carries operational risks, credit reporting implications, and the possibility of disputes if borrowers do not monitor their accounts carefully.

Safety ultimately depends on how you engage with the platform.

Verify every outstanding amount. Use only official payment channels. Monitor your credit report. Escalate issues early and formally.

Digital loans move fast. Your decisions should be made carefully.