Last week, a man in Mumbai lost ₹28 lakh to a trading app he found through a Telegram group.

A retired teacher in Kolkata invested her savings in a “guaranteed return” scheme that vanished overnight.

In Bengaluru, a scammer posing as a bank official tricked a young professional into sharing his OTP and wiped out his account within minutes.

Scammers use different methods in different cities, but they cause the same outcome.

Financial scams in India are no longer rare incidents buried in newspapers.

They are happening every single day, through fake investment platforms, IPO allotment promises, crypto schemes, phishing calls, loan apps, and even people claiming to be SEBI-registered experts.

And what makes them dangerous isn’t just the technology.

It’s how convincingly real they look.

Scammers don’t always appear suspicious. They sound professional. They display profits. By the time doubts arise, the money is already gone.

So the real question is not just “What is a financial scam?”

The real question is; How do these scams actually work? And how can you protect yourself before becoming the next headline?

Let’s break it down step by step.

What are Financial Scams?

Not every financial loss is a scam.

Markets fall. Businesses fail. Investments carry risk.

But a financial scam is different.

A financial scam involves intentional deception. It is when someone deliberately misleads you to take your money, by lying, hiding facts, fabricating returns, impersonating authorities, or creating a fake investment opportunity.

The key difference is intent.

If a stock falls because of market conditions, that’s risk.

If someone promises “guaranteed 30% monthly returns” knowing there is no real investment behind it, that’s fraud.

In most financial scams in India, the fraudster does one of three things:

- Pretends to offer a legitimate financial service

- Misrepresents returns or safety

- Uses false identity or fake credentials

Sometimes they claim to be investment advisors. Sometimes they pose as bank officials or create entire websites and apps that look professional.

But underneath the surface, there is no real business. No real profit. No real protection.

And the worst part?

Victims often realize it only after trying to withdraw their money.

To understand why so many intelligent, careful people fall for these traps, we need to look at something more important:

How financial scams actually work.

How Financial Scams Work?

If you remove the technology, the websites, and the polished language, most financial scams follow a very predictable structure.

They do not begin with theft. They begin with trust. Let’s understand the pattern.

1. Attraction

Every scam starts with something appealing.

It could be:

- Guaranteed 25% monthly returns

- Assured IPO allotment

- Crypto doubling schemes

- “Expert” stock tips with high accuracy

The promise always sounds better than regular investment options.

That is deliberate.

Scammers understand that high returns trigger curiosity. Curiosity lowers caution.

2. Trust Building

Once you show interest, they do not rush to take your money.

They build credibility first.

You may see:

- A professional-looking website

- Claims of registration or certifications

- Testimonials and profit screenshots

- A trading dashboard showing gains

- Frequent and polite communication

Sometimes they even allow small withdrawals initially. This stage is critical.

When you see profits or receive regular updates, your doubts begin to fade. The opportunity starts to feel real.

But the foundation is still fake.

3. Extraction: Encouraging Larger Investments

After building trust, the pressure begins.

You may hear statements like:

- “This opportunity is limited.”

- “Upgrade your plan for higher returns.”

- “Invest more to recover previous losses.”

- “The market window is closing.”

This is where victims usually invest larger sums.

The emotional shift is subtle. What started as curiosity becomes confidence. Confidence becomes commitment.

And that is where the trap tightens.

4. Exit: Withdrawal Blocked

The turning point often comes when the investor tries to withdraw funds.

Suddenly:

- Withdrawal requests are delayed

- Additional fees are demanded

- Accounts are frozen

- Customer support becomes unreachable

- The website or app disappears

The person who once called regularly stops responding. At this stage, the realisation sets in.

Financial scams in India are not just financial crimes. They are psychological strategies.

They rely on:

- Urgency

- Authority claims

- Social proof

- Fear of missing out

- Emotional pressure

That is why even educated and financially aware individuals can fall victim. Because the scam does not appear suspicious at the beginning. It appears convincing.

Now that we understand the pattern, let’s examine the different types of financial scams happening in India — along with real case studies that show how they unfold in reality.

Cases of Financial Scams in India

Financial scams in India have evolved beyond suspicious phone calls and random spam messages. Scammers now design structured, layered, and highly sophisticated schemes.

Sometimes they target individuals. Sometimes they trap entire investor groups.

And sometimes, even banks become victims.

Let’s look at real case studies to understand how these scams actually unfold, starting with a major bank fraud that exposed how vulnerable financial systems can be.

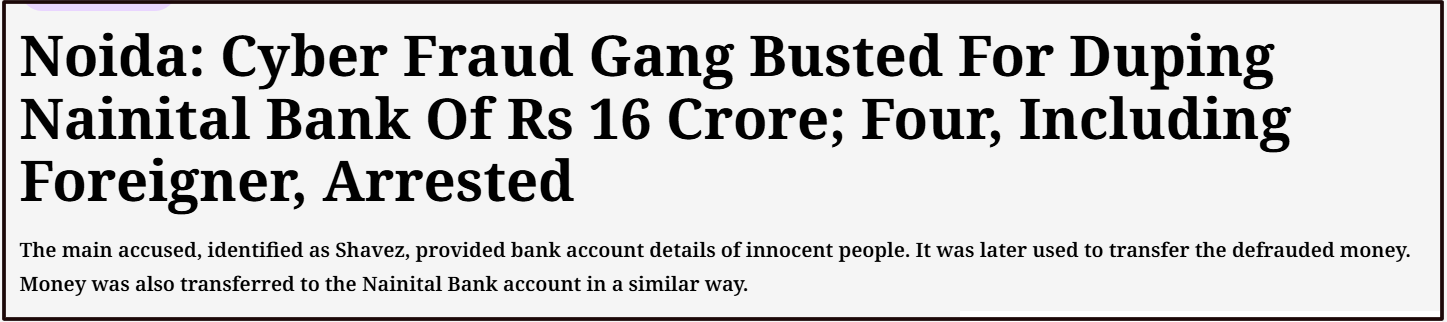

1. Nainital Bank Cyber Fraud

When we think of bank-related scams, we usually imagine customers being tricked into sharing OTPs. But in this case, the scammers targeted the bank itself.

Fraudsters siphoned off around ₹16.71 crore from Nainital Bank’s Noida branch in what was reported as a significant cyber fraud.

The amount itself was alarming, but what made it more concerning was how the breach reportedly occurred.

The breach was uncovered only after monitoring systems noticed irregular fund movements.

This screenshot confirms the scale of the fraud and the reported involvement of cybercriminals who allegedly gained unauthorised access to the bank’s systems.

It also mentions arrests made during the investigation, indicating that the matter escalated beyond a routine internal issue.

Unlike retail scams, this involved:

- Unauthorized access to internal banking systems

- Use of compromised login credentials

- Structured transfer of funds to avoid suspicion

- Delayed detection through layered transactions

This was not impulsive fraud. It required planning and technical knowledge.

What This Case Teaches?

- Cyber fraud is evolving beyond individual-level scams.

- Even regulated financial institutions are not immune.

- Detection often happens after funds are already moved.

- Recovery becomes complex once money passes through multiple accounts.

This case broadens our understanding of financial scams in India. They are not always about gullible victims; sometimes they involve deep systemic vulnerabilities.

2. Shah Investments

Investment scams rarely begin with something that looks illegal.

They usually begin with confidence.

In the case of Shah Investments, the firm projected itself as a professional investment consultancy. It used polished branding, social media promotions, and promises of attractive monthly returns to build credibility.

On the surface, everything appeared structured. That is what made it convincing.

Reports revealed that Shah Investments allegedly promised high fixed returns, around 5% per month, to investors.

This screenshot highlights the promises made and the concerns raised about the firm’s operations. It also reflects how the scheme relied heavily on digital marketing and trust-building strategies to attract investors.

What made the situation riskier was the lack of a verified SEBI registration.

Despite offering what appeared to be investment advisory or portfolio-related services, the entity did not have the regulatory backing expected for such financial activities.

This case followed a familiar pattern:

- Attractive monthly return promises

- Strong online presence and branding

- Confidence-building through communication

- Collection of funds from investors

- Limited transparency regarding actual investment deployment

Unlike a volatile market loss, this situation raised concerns of intentional misrepresentation, where returns were promised without verifiable underlying investment activity.

What This Case Teaches

- High fixed monthly returns should always be questioned.

- Professional branding does not equal regulatory legitimacy.

- Always verify SEBI registration independently.

- If a firm collects money without proper transparency, the risk increases significantly.

Investment scams are powerful because they look structured and respectable. They don’t appear desperate. They appear confident.

3. Maxizone Ponzi Scam

Ponzi schemes do not collapse on day one.

In fact, they often look the most successful in the beginning. Let’s check out a case here.

The Maxizone case is a classic example of how large-scale Ponzi structures operate across multiple states before eventually coming under investigation.

The scheme reportedly collected hundreds of crores by promising unusually high monthly returns, often between 10% to 20%.

That kind of return, especially on a fixed monthly basis, should immediately raise questions. But in reality, many investors were convinced.

This screenshot highlights the scale of the alleged fraud and the involvement of enforcement agencies.

It shows how authorities began investigating after large sums were mobilised from investors under the promise of consistent high returns.

The key issue was simple: there was no sustainable underlying business generating those returns.

The structure followed a typical Ponzi model:

- Promise of high, fixed monthly returns

- Rapid expansion through word-of-mouth and promotional events

- Payments to early investors using funds from new investors

- Continued inflow of money creating illusion of success

- Eventual collapse once new investments slowed

As long as fresh money kept coming in, the illusion remained intact.

But Ponzi schemes are mathematically unsustainable. Once inflow reduces, payouts stop.

What This Case Teaches?

- Fixed high monthly returns are a major red flag.

- Rapid expansion without regulatory clarity should be questioned.

- If returns depend on constant new investors, the structure is unstable.

- Early payouts do not prove legitimacy.

Ponzi schemes survive on confidence. The moment confidence breaks, everything collapses.

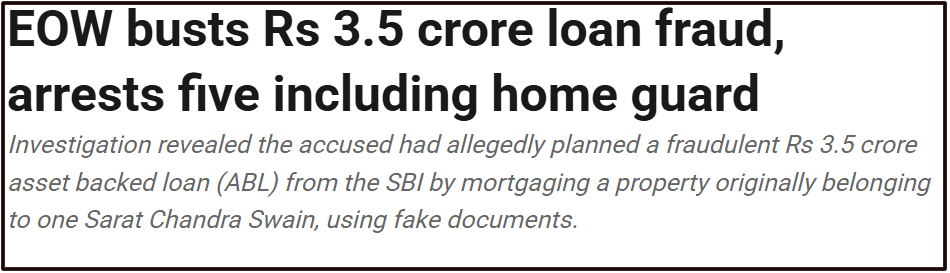

4. Bhubaneswar Loan Scam

Loan scams don’t target people who want to earn money. They target people who urgently need money.

The following case can be serves as an example here.

In Bhubaneswar, a loan fraud case surfaced involving around ₹3.5 crore. The accused allegedly lured victims by promising quick loan approvals, often without the usual formalities that traditional banks require.

For someone in financial stress, that promise can sound like relief.

This screenshot highlights the scale of the fraud and the arrests made during the investigation. It shows how multiple individuals were allegedly involved, indicating that the operation was organised rather than isolated.

In many such cases, once victims paid the upfront charges, the promised loan never materialised.

The pattern is common in loan fraud cases:

- Promise of fast loan approval

- Minimal documentation requirements

- Demand for upfront processing or insurance fees

- Repeated payment requests under different pretexts

- No actual loan disbursal

The urgency of the borrower becomes the scammer’s advantage.

What This Case Teaches?

- Legitimate banks do not ask for large upfront cash payments before disbursing loans.

- “Guaranteed approval” without credit checks is a warning sign.

- Pressure to pay quickly to secure loan approval should be questioned.

- Always verify the lender’s regulatory registration and physical presence.

Loan scams exploit vulnerability. They appear helpful at first, but they operate purely to extract money.

5. Fake Trading App Scams

Fake trading apps are among the fastest-growing financial scams in India today.

They look real. They show profits and even allow small withdrawals in the beginning.

But the numbers you see are not connected to any real market.

In one reported case from Thane, a senior manager allegedly lost around ₹88 lakh after joining a WhatsApp group that promoted stock trading opportunities. What began as casual participation turned into a major financial loss.

Reports indicate that the victim was added to a WhatsApp group where market insights and profit screenshots were regularly shared.

The group appeared active and professional, building credibility over time.

This screenshot highlights the scale of the loss and how the victim was persuaded to download a trading app. The app displayed impressive profits, reportedly even showing figures as high as ₹2.79 crore on the dashboard.

But those profits were only numbers on a screen.

When the victim attempted to withdraw funds, additional payments were demanded. Eventually, withdrawals were blocked completely.

The structure followed a calculated path:

- Addition to WhatsApp investment group

- Regular sharing of fake profit screenshots

- Encouragement to download a specific trading app

- Initial small profits displayed to build confidence

- Gradual increase in deposits

- Withdrawal blocked unless “additional charges” were paid

The trading interface looked authentic, but it was not connected to any legitimate exchange.

What This Case Teaches?

- Being added to an investment WhatsApp group is not proof of legitimacy.

- Trading apps not verified on official platforms should be avoided.

- Large profits displayed quickly are often fabricated.

- Withdrawal restrictions are a major red flag.

Fake trading app scams rely heavily on visual manipulation. The dashboard becomes the tool of deception.

6. ₹21 Crore Cryptocurrency Fraud in Sriganganagar

Cryptocurrency scams often operate in a grey zone.

They combine technical language, digital wallets, and high-return promises, making it difficult for ordinary investors to understand what is real and what is fabricated.

In Sriganganagar, a major cryptocurrency fraud surfaced involving around ₹21 crore. The scale itself shows how convincing such schemes can be when packaged professionally.

According to reports, investors were lured with promises of high returns through cryptocurrency investments.

The scheme reportedly projected itself as a structured digital asset opportunity, attracting people who wanted to participate in the crypto boom.

This screenshot highlights the amount involved and the investigation initiated by authorities.

It reflects how large sums were mobilised before action was taken. Arrests and enforcement steps followed, but as seen in many such cases, recovery becomes complex once funds are moved digitally across wallets and accounts.

The core issue was not cryptocurrency itself; it was the misuse of the crypto narrative to build trust.

The structure typically involved:

- Promise of high returns through crypto trading or mining

- Use of technical jargon to create authority

- Collection of funds from multiple investors

- Movement of funds through digital wallets

- Disappearance or inability to provide withdrawals

Crypto platforms allow fast fund movement, which makes tracing and recovery more challenging.

What This Case Teaches?

- High guaranteed returns in crypto are unrealistic.

- Technical complexity is often used to discourage questioning.

- Lack of regulatory clarity increases risk.

- Once funds move through digital wallets, recovery becomes difficult.

Crypto scams thrive on hype and complexity. Investors often assume that digital equals innovative, but in many cases, it simply means harder to trace.

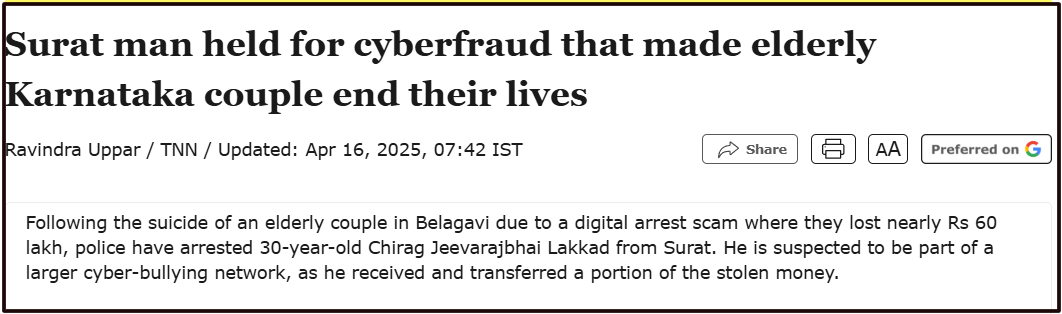

7. Digital Arrest Scam

Not all financial scams begin with profit promises.

Some begin with fear.

In recent years, so-called “digital arrest” scams have emerged, where fraudsters impersonate law enforcement officers, cybercrime officials, or government agencies.

Victims are told they are involved in money laundering, illegal transactions, or criminal investigations.

The pressure is immediate. The tone is authoritative. And the objective is simple; make the victim transfer money “for verification” or “to avoid arrest.”

In cases linked to the broader cryptocurrency and online fraud investigations, digital intimidation tactics have also been reported, where victims were forced to stay on video calls while funds were being transferred.

Reports indicate that victims were contacted through phone or video calls by individuals posing as officials. They were shown fake ID cards, legal notices, or case documents to create authenticity.

This screenshot highlights the seriousness of the allegations and the scale of funds involved. It reflects how psychological pressure was used to control victims during the transfer process.

The most dangerous part of a digital arrest scam is not technology, it is authority impersonation.

The typical structure includes:

- A call from someone claiming to be from police, CBI, ED, or cybercrime

- Accusation of involvement in illegal financial activity

- Threat of arrest or legal action

- Instruction to transfer funds for “verification”

- Continuous monitoring of victim through video call

Victims are often isolated during the call to prevent them from consulting family or friends.

What This Case Teaches?

- Law enforcement agencies do not demand money over video calls.

- Immediate threats combined with secrecy instructions are major red flags.

- No genuine investigation requires instant online fund transfers.

- Fear-based urgency is a common psychological manipulation tactic.

Digital arrest scams are growing because they do not rely on greed, they rely on fear.

8. Darshan Orna SEBI Telegram Case

Telegram has become a popular platform for financial communities.

But it has also become a fertile ground for investment-related scams.

In the Darshan Orna case, authorities examined activities conducted through Telegram channels where investment advice and stock recommendations were allegedly circulated without proper regulatory compliance.

The matter escalated to regulatory action, with significant monetary penalties imposed.

The case highlights how messaging platforms are increasingly used to mobilize investors quickly and at scale.

Reports suggested that the individuals involved used Telegram groups to share stock-related recommendations and build a following.

The communication appeared structured, regular, and confident, creating an impression of expertise.

This screenshot reflects the regulatory action taken and the seriousness of the violations.

It demonstrates that unauthorized solicitation of investment advice through social media platforms can attract penalties, especially when regulatory norms are not followed.

Unlike traditional scams that disappear quickly, Telegram-based schemes often operate in closed groups where trust builds gradually.

The pattern typically involves:

- Creation of Telegram groups with financial themes

- Sharing of stock tips or “exclusive” recommendations

- Display of profit screenshots to build credibility

- Collection of subscription fees or indirect gains

- Lack of transparent regulatory compliance

Closed groups create a sense of exclusivity. Members see others reacting positively, which strengthens belief in the operator’s credibility.

What This Case Teaches?

- Social media popularity does not equal regulatory approval.

- Investment advice requires proper registration and compliance.

- Telegram groups can amplify misinformation quickly.

- Always verify credentials independently before acting on financial tips.

Financial scams in India are evolving with technology. From bank cyber breaches to Telegram-based advisory violations, the common thread remains the same, trust is built first, money is taken later.

Now that we have examined different types of scams through real case studies, the next important question is:

What should you do if you become a victim?

How to Report a Financial Scam?

When a financial scam happens, most victims freeze.

That delay can cost recovery time.

If you suspect that you have been targeted in a financial scam in India, here are the immediate steps that matter.

1. Act Immediately

Time is critical.

If the fraud involves an online transaction, call National Cyber Crime Helpline, as soon as possible. Early reporting increases the chances of freezing the transferred funds before they are layered into multiple accounts.

2. Report on the Cyber Crime Portal

File a complaint at the official National Cyber Crime Reporting Portal.

Provide:

- Transaction details

- Account numbers involved

- Screenshots of chats or apps

- Bank statements

- Call logs

The more precise your documentation, the stronger your case becomes.

3. Inform Your Bank Immediately

Notify your bank in writing and request:

- Transaction reversal attempt

- Temporary account freeze (if needed)

- Dispute registration

If the fraud involves a banking error or unauthorized debit, banks have defined grievance mechanisms and timelines.

4. Approach SEBI for Investment-Related Scam

If the fraud involves:

- Stock tips

- Portfolio management

- Trading apps

- Advisory services

You can file a complaint on the SEBI SCORES portal.

Regulatory bodies cannot always recover money instantly, but they can initiate action against unauthorized operators.

5. Preserve All Evidence

Do not delete:

- WhatsApp chats

- Telegram messages

- Email communication

- App dashboards

- Payment confirmations

Scammers often delete accounts later. Your saved evidence becomes crucial.

Reporting is not just about recovery.

It helps authorities identify patterns, trace networks, and prevent others from becoming victims.

Need Help?

When someone loses money in a financial scam, the first reaction is shock. The second is hesitation.

Many victims delay action because they feel embarrassed or unsure about the process. But delay reduces the chances of recovery.

Over time, we have helped victims across different types of financial scams, including, Misleading investment advisors, Unauthorized trading and broker disputes, Fake trading app losses, Crypto-related fraud and also Advisory fee disputes.

Recovery does not happen automatically. It requires proper documentation, correct complaint filing, and consistent follow-up with authorities or regulators.

Here’s how we help:

- We carefully review your case

- We help organize transaction proofs and communication records

- We draft structured complaints

- We guide you through SEBI, exchange, bank, or cybercrime processes

- We follow up until the matter reaches a logical resolution

In several cases, victims have been able to recover partial or significant portions of their funds by taking timely and structured action.

If you have been affected, don’t assume the money is permanently lost.

You can register with us, and we will guide you step-by-step through the recovery process.

Conclusion

Financial scams in India take many forms, from cyber breaches in banks to Ponzi schemes, fake trading platforms, and misleading investment advice. The one thing they all share is the exploitation of trust and human psychology.

But knowing how these scams work, where to report them, and how to pursue recovery can make a real difference.

Early action, strong evidence, and persistent follow-up can turn a fearful situation into an opportunity for accountability and partial; or even full, recovery.

If you’ve been affected, don’t stay silent. Report it, document it, and take the next step toward reclaiming what’s rightfully yours.

You are not alone; help is available.