Is Fincare Capital safe to use for wealth advisory and investment services? It claims a 12-year track record, serves clients across Bengaluru and Hyderabad, and presents a polished, professional website.

But several inconsistencies in their own public documents and app store disclosures raise questions that every investor should ask before proceeding.

Here is what the research actually shows.

Fincare Capital Review

Fincare Capital Management Services LLP is a Hyderabad and Bengaluru-based wealth advisory and investment services company established in 2012.

The firm offers financial planning, mutual fund distribution, wealth management, and investment advisory across individuals, families, NRIs, trusts, and MSMEs.

It also runs a mobile app on both Google Play and Apple App Store.

Is Fincare Capital Registered?

Fincare Capital operates under NSE Member Code MFS88253 and BSE Member Code 20980, and holds AMFI registration as a Mutual Fund Distributor under ARN 88253.

These confirm that it operates as a registered mutual fund distributor, meaning it earns commission from distributing mutual fund products.

However, no SEBI Research Analyst (RA) or Investment Adviser (IA) registration number appears anywhere on the website, the app store listing, or any public disclosure.

This distinction matters significantly. A mutual fund distributor earns commission from the products it sells, it does not provide independent, fee-based investment advice regulated under SEBI’s IA or RA framework.

Investors who approach Fincare Capital expecting independent, unbiased research or personalised investment advice must understand that the firm’s registration does not cover those functions.

Is Fincare Capital Safe or Not?

So is Fincare Capital safe? The firm is a registered mutual fund distributor whose baseline is confirmed.

But several inconsistencies in its own disclosures raise specific concerns that investors cannot ignore.

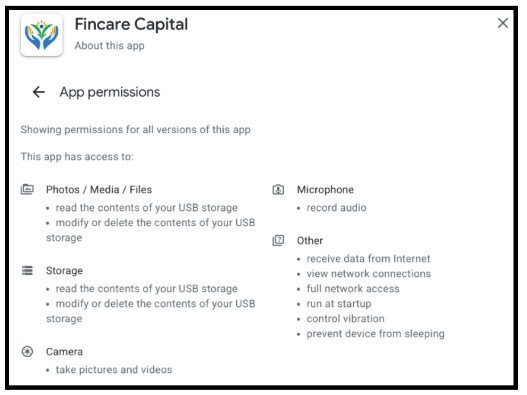

1. Excessive Data Collection

The overall scope of data the app collects, when you examine what the app actually requests access to, goes beyond what a mutual fund distribution service functionally requires.

A platform that helps clients track mutual fund portfolios and plan financial goals does not need access to the range of data points the app appears to request.

Excessive data collection in a financial context creates a privacy risk that investors should consciously factor in before granting permissions.

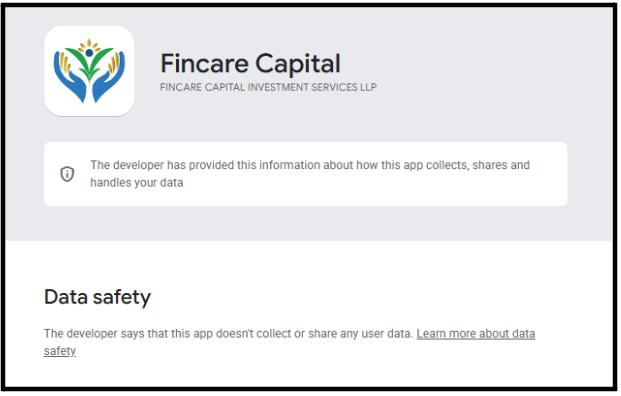

2. Google Play Store Says “No Data Collected,” But the App Requests Permissions

The Google Play Store Data Safety section for the Fincare Capital app clearly states: “No data collected.”

However, when installed, the app requests access to device permissions that typically accompany data collection.

The developer declares one thing publicly while the app behaves differently in practice.

For a financial services app where users log in with personal and investment details, this gap between declaration and behaviour is a concern worth investigating before installing.

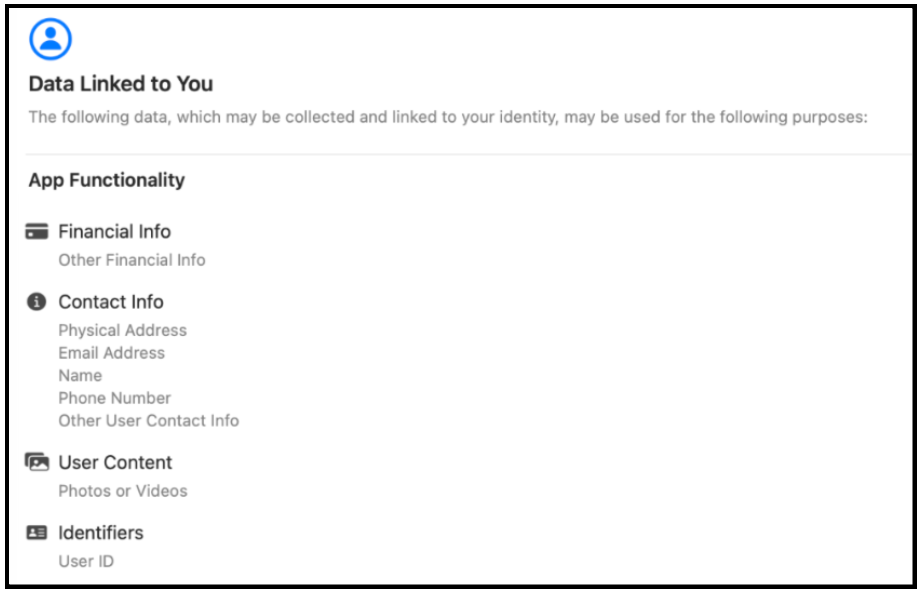

3. Data Collection Practices Differ Between Google Play and App Store

The same Fincare Capital app shows different data practices across platforms.

Apple’s App Store enforces stricter privacy disclosure requirements, and the app’s declared practices there differ from what appears on Google Play.

A genuine financial services app should maintain identical, transparent data practices regardless of platform.

When the same app declares different things on different stores, it raises a straightforward question about which declaration is accurate.

4. Zero User Reviews

The Fincare Capital app shows 1,000+ downloads on Google Play but carries zero user reviews: no ratings, no comments.

Apps with over 1,000 downloads almost always accumulate some public feedback. The complete absence of reviews means there is no independent public record of the user experience.

A prospective user cannot assess app functionality, support quality, or service reliability from other users’ experiences, which matters significantly for a platform handling investment data.

5. Website Disclaimer Contradicts the Services Page

The website footer disclaimer states explicitly: “This site should not be treated as a financial advisory website and this site does not suggest or recommend any specific scheme.”

Yet the About Us page and Services page describe the firm as providing “investment advisory,” “wealth advisory,” and “portfolio solutions.”

A first-time visitor reading the services page gets one impression of what the firm offers. A careful reader who finds the footer disclaimer gets the opposite.

For a financial services firm, that internal contradiction creates genuine consumer confusion about what service the client is actually receiving and under what regulatory framework.

What Investors Must Keep in Mind?

Is Fincare Capital safe to engage with? Its AMFI registration is real, and its commission structure is disclosed.

But the data practices across platforms, the app permission questions, and the internal website contradiction mean that going in with eyes open is more important than the registration alone suggests.

- Understand that AMFI registration covers mutual fund distribution, not independent investment advice

- Read the footer disclaimer carefully; it tells you more about what this service actually is than the services page does

- Check what permissions the app requests before installing and decide whether those permissions match what you expect a mutual fund distributor to need

- The absence of user reviews means you cannot rely on public feedback to assess service quality before committing

Fincare Capital earns commission from the mutual fund products it distributes, not from your investment returns.

That commission structure shapes which products the firm recommends, whether intentionally or not.

Before investing through any commission-based distributor, always ask which fund they are recommending and what commission they earn from it.

That question costs nothing and tells you a great deal. Is Fincare Capital safe? It is ultimately a question about whether you go in informed, and now you have the information to do that.

What To Do In Such Cases?

If you engaged with Fincare Capital, invested based on their recommendations, and faced losses or service issues that were not adequately addressed, here is how to proceed.

- Keep Your Records: Save everything: payment receipts, bank records, chats, calls, and any tips or messages. This is your proof.

- Contact Fincare Capital First: Send a clear email explaining your issue, what was promised, and what went wrong. Keep their reply (or no reply) as evidence.

- File a complaint with AMFI: Since Fincare Capital has AMFI registration (ARN 88253), file a complaint on amfiindia.com. Attach all proofs of mis-selling or issues.

- Report Cyber Crime: If you feel cheated or scammed, file a complaint on the National Cyber Crime Portal. This covers online financial fraud.

- File a Complaint with SEBI: Since Fincare Capital is not SEBI-registered, SCORES is not the right channel. Instead, write an email directly to SEBI’s Investor Complaints Cell with your details, the firm’s name, the nature of the complaint, and supporting evidence. SEBI can initiate an inquiry or enforcement action against unregistered entities.

- Take Legal Help: For big losses, consult a lawyer. You can also go to the Consumer Court under the Consumer Protection Act.

Navigating these steps alone, while dealing with financial stress, can be overwhelming. If you are unsure where to begin or want someone experienced to handle your case end-to-end, register with us today.

Conclusion

Is Fincare Capital safe? It holds a valid AMFI registration, discloses its commission structure publicly, and has operated since 2012. Those are genuine positives.

At the same time, contradictions like “no data collected” vs actual permissions, inconsistent disclosures, and excessive data access raise concerns.

Zero reviews and a website that denies advisory while selling it are red flags investors should not ignore.

None of them is a regulatory violation in isolation. Together, they represent a gap between how the firm presents itself and what the fine print actually says.

That gap is what every investor must close before sharing their financial data or following a distributor’s recommendations.