Lemonn has recently come under discussion due to concerns raised by investors regarding trading execution and account handling practices.

In regulated markets, transparency, proper authorization, and clear communication between brokers and clients are essential.

When trading activities happen without clear consent or when there is confusion around margin usage and order execution, questions naturally arise.

Investors expect full visibility into how their trades are managed and how positions are executed.

This blog aims to explain key concepts, regulatory expectations, and important factors related to trading operations under the Lemonn platform, with clarity and factual understanding in mind.

In this blog, we will focus on information and awareness, not allegations or disputes.

Lemonn Trading

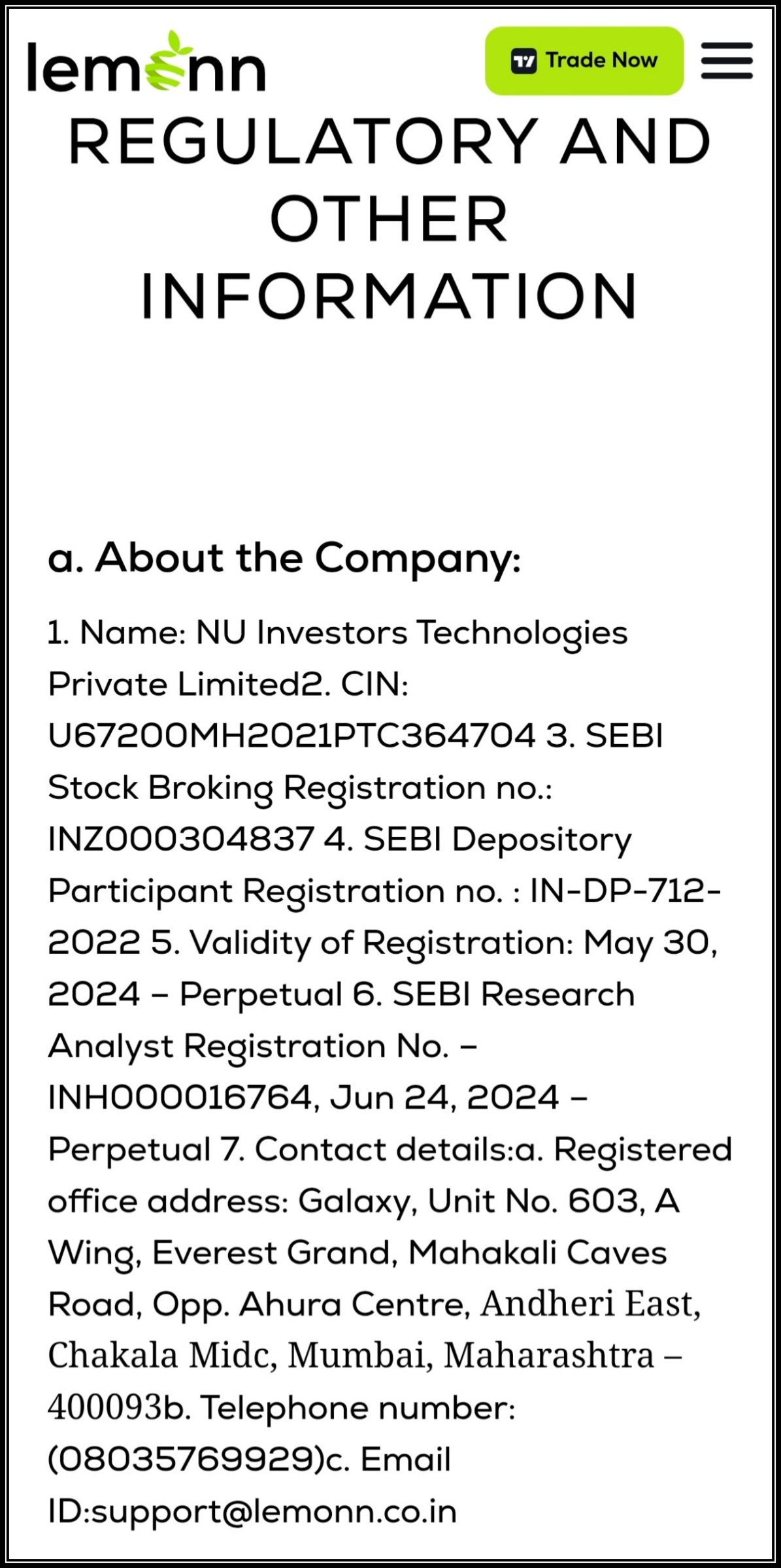

Lemonn operates under the entity NU Investors Technologies Private Limited, which is registered with SEBI as a stock broker and depository participant. The company’s regulatory details are publicly disclosed on its website.

The following screenshot reflects the regulatory information section as displayed on the official website:

The screenshot above shows the official regulatory disclosures of NU Investors Technologies Private Limited, which operates the Lemonn platform.

The details visible include SEBI Registrations:

- Stock Broking Registration No: INZ000304837

- Depository Participant Registration No: IN-DP-712-2022

- Research Analyst Registration No: INH000016764

The details are true as compared to the data available on the official databases.

These registrations confirm that the entity is authorised to operate as a stockbroker and depository participant under SEBI regulations.

However, SEBI registration does not eliminate the obligation to follow strict compliance norms.

A registered broker must:

- Obtain clear client consent before executing trades

- Disclose risks involved in derivatives trading

- Clearly communicate margin exposure

- Avoid misleading return projections

- Maintain proper documentation of trade authorisation

If a relationship manager handles trades without informed consent, or if risk and margin exposure are not properly explained, such actions may raise regulatory concerns, even if the broker itself is registered.

Registration allows a broker to operate. It does not remove the obligation of transparency and consent.

What Is Unauthorised Trading?

Unauthorised trading is not simply about loss.

It generally refers to situations where:

- Trades are placed without the client’s explicit consent

- Higher quantities are executed than instructed

- Risk and margin exposure are not properly explained

- Dealer terminals are used without proper recorded authorisation

- Churning in stock market

Loss alone does not prove misconduct. But loss, combined with the absence of consent and disclosure, raises regulatory questions.

How To File a SEBI Complaint Against a Stock Broker?

If the broker’s internal grievance process does not resolve the issue, you can escalate the matter through regulatory channels. The process is structured and documentation-based.

1. Raise an Internal Complaint First

Before approaching SEBI, you must submit a written complaint to the broker’s official grievance redressal officer.

Clearly mention:

- The trades you are disputing

- Quantity mismatch (if any)

- Lack of risk or margin disclosure

- Timeline of events

- Supporting documents attached

Keep a copy of your complaint email and the response received. Brokers are required to respond within a defined timeframe.

2. File a Complaint on SEBI SCORES

If the issue remains unresolved, you may register a complaint on the SEBI SCORES (SEBI Complaints Redress System) portal.

While filing the complaint:

- Select the correct intermediary category (Stock Broker)

- Enter the broker’s name and registration details

- Provide a clear and chronological explanation of events

SEBI evaluates complaints based on documented evidence, especially whether trades were authorised and risks were disclosed.

3. Escalate to the Exchange

If required, the matter can be escalated to the respective stock exchange (NSE/BSE) grievance redressal mechanism.

The exchange may review:

- Order logs

- Recorded authorisation

- Margin exposure

- Compliance with trading norms

In certain cases, disputes may proceed to arbitration under the exchange framework.

4. File Arbitration in the Stock Market

If the grievance remains unresolved, arbitration through the exchange mechanism is an option.

Arbitration examines:

- Whether trades were placed with consent

- Whether risk and margin disclosures were adequate

- Whether brokerage practices complied with regulations

This is a more formal process and relies heavily on documentation.

Need Help?

If you have any issues with your broker, you do not have to navigate it alone.

Register with us and we will assist you in:

- Reviewing trade documents and contract notes

- Organising communication and payment records

- Structuring complaints clearly and chronologically

- Identifying relevant regulatory provisions

- Preparing submissions to brokers, exchanges, or SEBI

Conclusion

Allegations of unauthorised trading are serious in any regulated financial environment.

Lemonn operates as a SEBI-registered broker, and with that registration comes strict obligations, including obtaining proper client consent, clearly explaining risk, disclosing margin exposure, and maintaining transparent trading practices.

Markets involve risk. But informed consent, transparency, and accountability are not optional; they are foundational to a regulated system.

When clarity is missing, documentation becomes the investor’s strongest safeguard.