Quick Summary

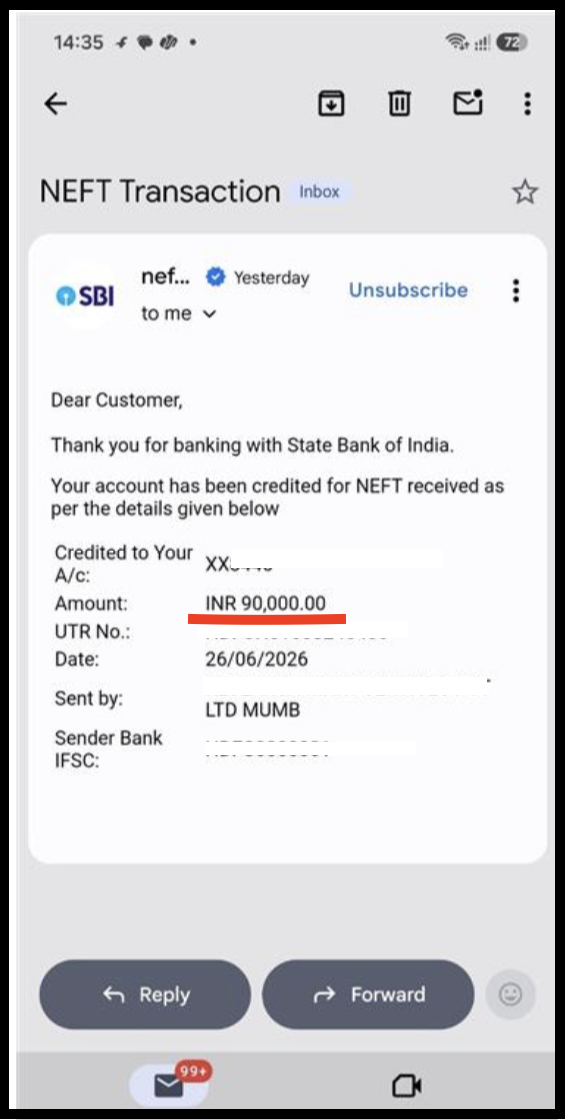

A stock advisory refund is not one number. It splits into two very different parts, and they behave in opposite ways. The fees you paid the firm tend to come back. The money you lost trading on their calls usually does not. In one settled case, a client claimed 6,60,500 and recovered 90,000. In another, a client claimed 7,00,000 and recovered 5,00,000. Both were research analyst cases. Both settled. The difference was not luck. The second client had paid most of that claim as fees. The first had lost most of it in the market. That single ratio, fees against trading loss, shapes what you can realistically expect.

You paid an advisory firm 30,400 in fees. You then lost 34,000 trading on their calls. Your total damage is 64,400, and that is the number in your head.

But a stock advisory refund does not work on that total. It works on the two halves separately, and one half is far easier to recover than the other.

Most people find this out after they file.

They claim the full amount, expect the full amount, and then hear a settlement figure that looks like a fraction of what they lost. It is not arbitrary. It follows a pattern you can work out for yourself in about two minutes.

Here is what that pattern looks like across five settled cases.

Stock Advisory Refund Cases: What Five Settlements Show

These are five real cases. All five settled. All five involved a firm that was, or claimed to be, registered with SEBI as a research analyst or investment adviser.

The table below is sorted by one thing only: how much of the claim was fees versus trading loss.

Read it from top to bottom and the pattern appears without anyone pointing at it.

| Fees paid | Trading loss | Total claimed | Recovered | Share of claim |

|---|---|---|---|---|

| 10,500 | 6,50,000 | 6,60,500 | 90,000 | 13.6% |

| 26,999 | 2,50,000 | 2,76,999 | 80,000 | 28.9% |

| 4,87,500 | 4,00,000 | 8,87,500 | 3,35,000 | 37.7% |

| 2,95,000 | 2,11,000 | 4,22,000 | 3,00,000 | 71.1% |

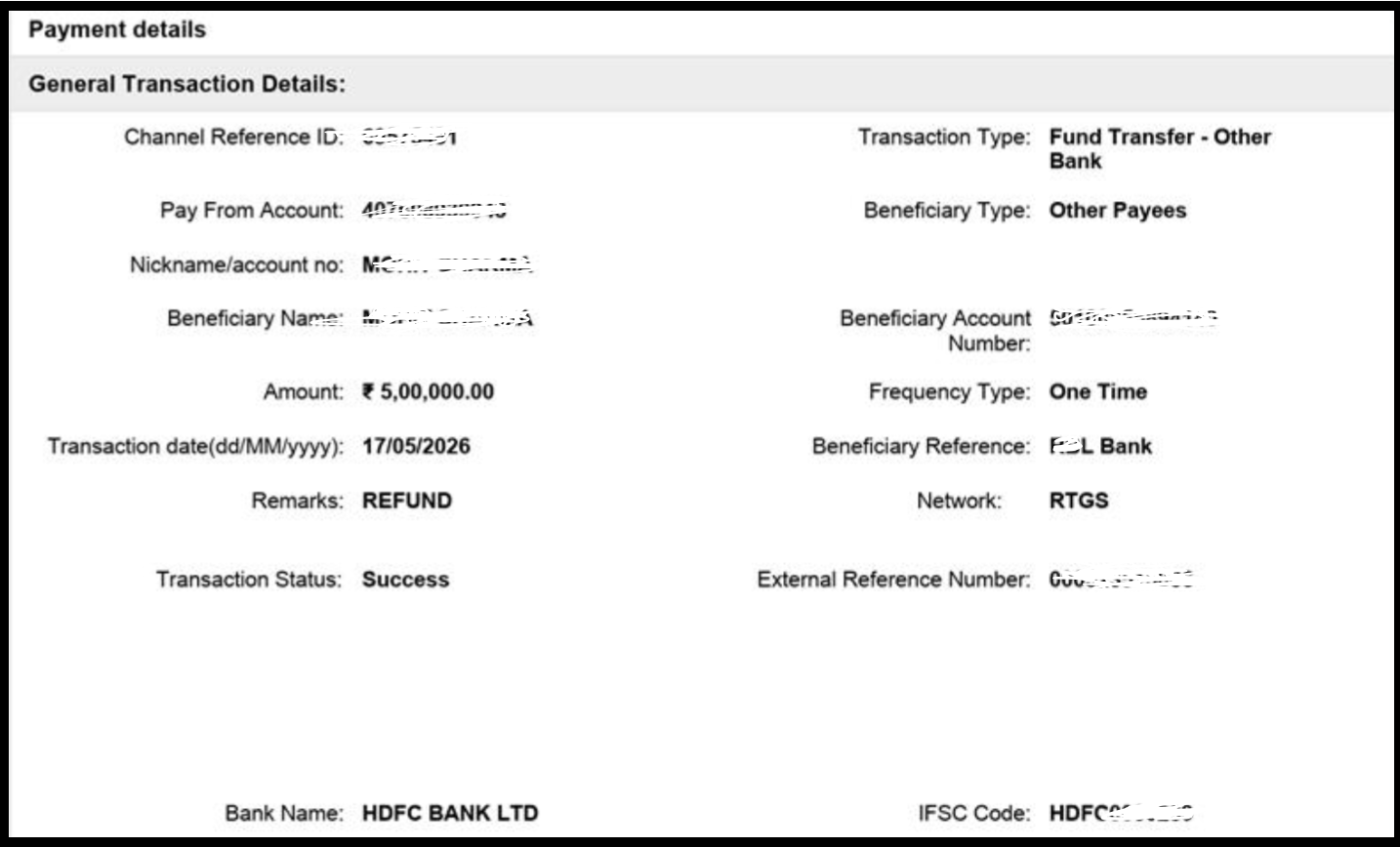

| 5,00,000 | 2,80,000 | 7,00,000 | 5,00,000 | 71.4% |

Look at the first row and the last row.

The client in the first row lost 6,50,000. The client in the last row lost 2,80,000, less than half as much. Yet the second client walked away with 5,00,000 and the first with 90,000.

The first client had paid 10,500 in fees. The last had paid 5,00,000.

The recovery tracked the fees, not the loss.

Why Advisory Fees Refund Faster Than Trading Losses

The reason is not sympathy or negotiation skill. It is evidence.

A fee is a transaction. There is an invoice, or a bank transfer, or a UPI record. Money moved from your account to theirs on a specific date for a specific stated service. Nobody can argue about whether it happened. The only argument left is whether the service was delivered as promised, and that is an argument you can win with chat records and call recordings.

A trading loss is an interpretation. You bought a position, the market moved, the position lost money. To recover that, you have to establish that the loss was caused by the firm’s advice rather than by the market, and that the advice itself breached what a registered firm is permitted to do.

That second argument is winnable. But it is slower, it depends on the quality of your records, and it rarely recovers the full amount.

So a claim that is mostly fees is mostly documented. A claim that is mostly trading loss is mostly argued. That is the whole mechanism.

It also explains why two clients with similar losses can end up with completely different outcomes.

Research Analyst Fee Refund When the Loss Is Large: A 13.6% Case

This client paid 10,500 to a SEBI registered research analyst.

The approach was familiar. A phone call. A demo trade to build trust. A stated fee of 40,000, dropped to 10,500 when the client hesitated, which made the smaller number feel like a concession rather than a hook.

After the payment, the trading calls started. One early trade made money. Then the losses began.

The client asked to exit. They were told to hold. Positions were recommended in quantities the client had not been assessed for. One single trade lost roughly 1,25,000. The total trading loss reached 6,50,000.

The claim was 6,60,500. The recovery was 90,000.

Run the arithmetic. The recovery is roughly nine times the fee. In pure fee terms, this client did well. But the fee was 1.6% of the claim, so the outcome looks like a failure on the headline number.

This is the case that teaches the lesson. If almost all of your damage is trading loss, the honest expectation is a partial outcome, and you should know that before you start rather than after.

Can I Get My Advisory Fees Back in Full? A 71.4% Case

Now the other end.

This client was contacted in March 2026 by two representatives selling call based trading tips. They showed profits supposedly earned by older clients. A demo trade showed a small profit. The client subscribed.

Over eight days, the client paid roughly 5,00,000 in service fees.

The trading advice was specific. Exact instructions on how many lots to buy. When positions moved against the client, the instruction was to hold and avoid a stop loss. When losses grew, the client was pushed to add funds on the assurance that the losses would come back.

The trading loss reached 2,80,000. The claim was 7,00,000. The recovery was 5,00,000.

Note what happened. The client recovered an amount equal to the fees, near enough. The trading loss largely stayed with the client.

That is the pattern in its clearest form. The fees came back. The loss mostly did not.

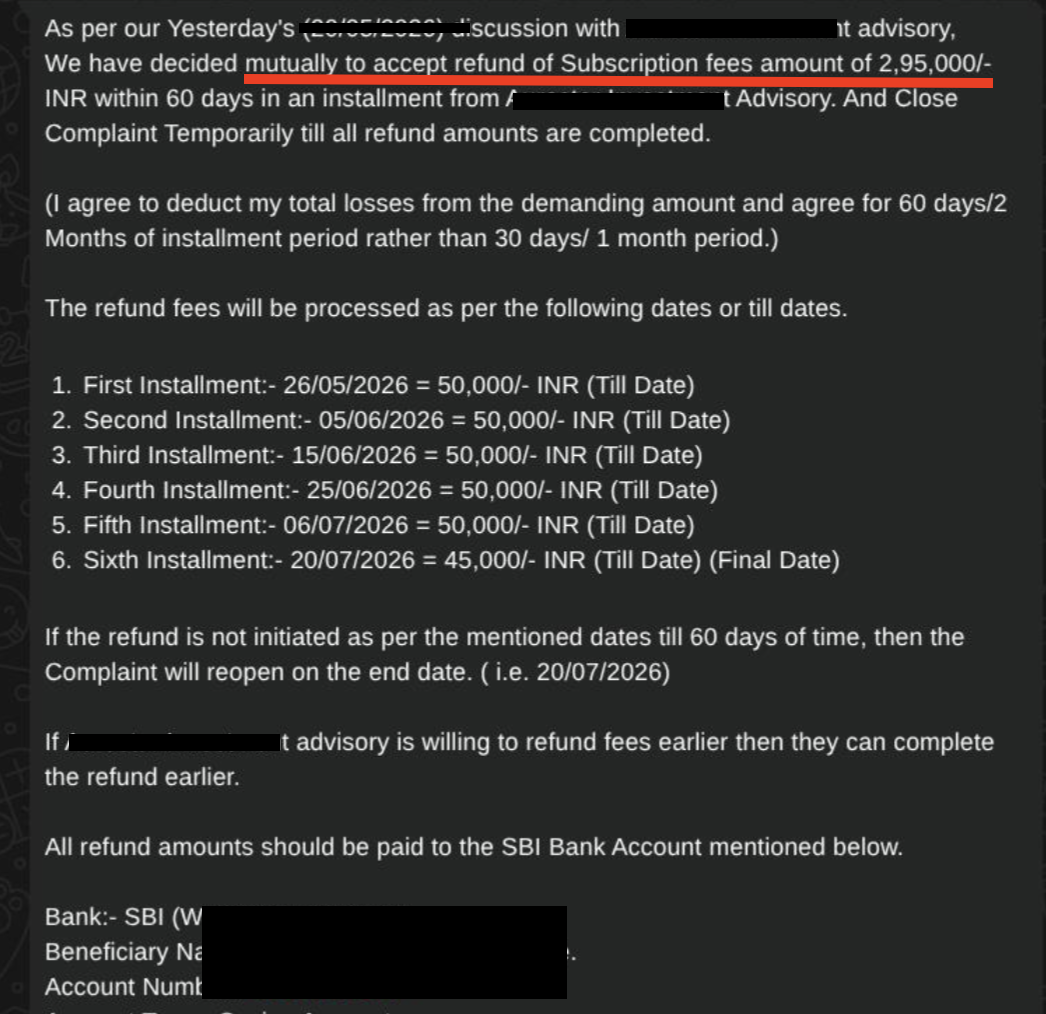

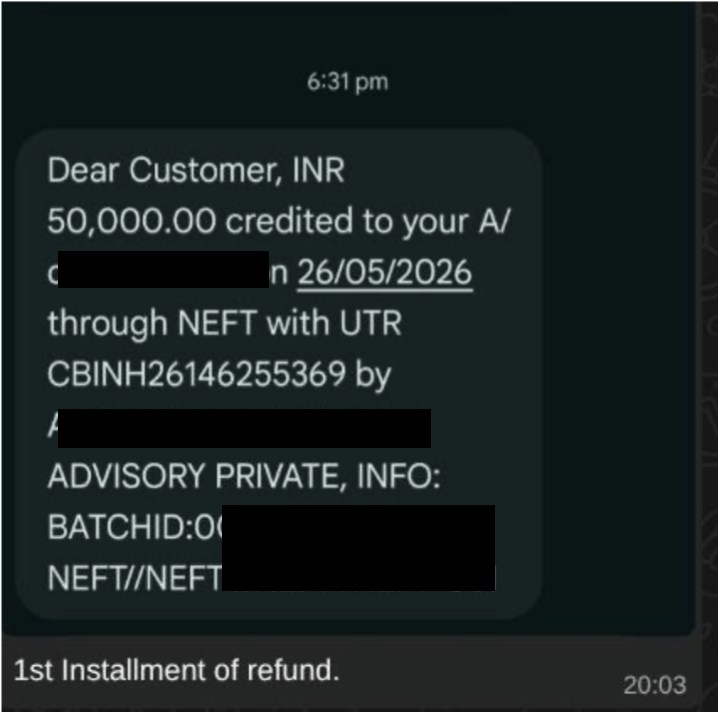

The same shape appears in a separate investment adviser case. That client paid 2,95,000 in fees, lost 2,11,000 trading, claimed 4,22,000 and recovered 3,00,000. Fee heavy claim, high recovery.

Work Out Your Own Stock Advisory Refund Ratio

You can do this yourself right now, and it takes two minutes.

Add up every rupee you paid the firm directly. Subscription fees, package upgrades, renewal charges, anything that left your account and went to them. That is your fee number.

Then add up what you lost in the market trading on their calls. That is your loss number.

Divide the fee number by the total. That percentage is the strong part of your claim.

A client with 5,00,000 in fees and 2,80,000 in losses has a claim that is 64% fees. A client with 10,500 in fees and 6,50,000 in losses has a claim that is 1.6% fees.

Those are not the same case, and they should not carry the same expectation. Knowing which one you are is the difference between a realistic filing and a disappointed one.

A third client sat between the two. They paid 4,87,500 in fees and lost 4,00,000 trading. The claim was 8,87,500 and the recovery was 3,35,000, which is 37.7%. Roughly 55% of that claim was fees, and the outcome landed in the middle of the range.

This does not mean a loss heavy claim is not worth filing. Every case in the table above recovered something. It means you should file knowing what the shape of your claim is.

Not sure how much of your claim is actually recoverable?

We separate your fees from your trading losses, work out what each part is worth, and tell you the realistic number before you file anything.

Register with us for a free consultation.

What Makes a Trading Loss Refundable From an Advisory

The trading loss is harder. It is not impossible.

What moves it is proof that the firm did something a registered entity is not permitted to do. Not that you lost money. That the loss came from conduct the rules prohibit.

Across these five cases, the same conduct kept appearing.

Personalised trade instructions from a research analyst. A registered research analyst is permitted to publish research. Telling a specific client to buy a specific quantity of a specific stock at a specific time is not research. It is account management, and it sits outside what a research analyst registration allows.

Refusing to give a stop loss when the client asked for one. The rules require risk disclosure before a recommendation. A refusal, in writing, is evidence.

Pushing the client to add capital after a loss on the assurance of recovery. No registered firm may assure you of a recovery. That assurance, on a call recording or in a chat, is one of the strongest things you can hold.

Showing other clients’ profit screenshots without any risk disclaimer. Past performance shown without prescribed disclosures is a documented breach, not a matter of taste.

Charging fees linked to how much capital you had, rather than to the service provided.

Each of these turns “I lost money” into “I lost money because of something the firm was not allowed to do.” That is the sentence that moves a trading loss from unrecoverable to arguable.

If any of these happened to you, the loss half of your claim is worth pursuing rather than writing off.

Records You Need for an Advisory Fees Refund in India

Your recovery depends less on how much you lost and more on what you can prove. The five cases above all had documentation. That is not a coincidence.

- Payment records come first. Bank statements, UPI transaction records, credit card statements, invoices if you were given any. Several of these clients were never issued an invoice at all, which is itself a compliance failure worth citing. Your bank record still proves the payment.

- Chat records matter more than people expect. The instruction to hold. The refusal to give a stop loss. The push to add funds. The profit screenshots. In most of these cases the entire relationship ran on WhatsApp, which means the whole record sits on the client’s phone.

- Call recordings are the strongest single item, and the rarest. In the 71.4% case and in another, recordings captured the specific assurances. If you have even one, it changes the weight of your file.

- Account statements show what was actually traded, in what quantity, and when. They connect the instruction to the trade.

Do not wait to gather these. Chat histories get deleted. Numbers stop working. In one of these cases the representative’s phone number was unreachable within months. Export what you have now, before you file anything.

The route you file through, whether that is a SEBI SCORES complaint or SMART ODR, depends on the entity type and what you are claiming. The evidence you carry into it is the same either way.

Conclusion

Stop thinking about your loss as one number.

Split it in two. Fees on one side, trading loss on the other. The fee side is documented and it is the part these five cases consistently recovered. The loss side is arguable, it takes evidence of specific prohibited conduct, and it recovers partially when it recovers at all.

Work out your ratio before you do anything else. A claim that is 64% fees and a claim that is 1.6% fees are different cases with different realistic outcomes, even if the headline damage looks similar.

Then pull your records together while they still exist. The outcome in every case above was decided by what the client could prove, not by how much they had lost.

Frequently Asked Questions

Yes. Several of these clients were never issued one. Your bank or UPI record proves the payment happened, and the absence of an invoice is itself a failure the firm has to answer for. It weakens their position, not yours.

It changes the route more than the outcome. A registered firm can be taken through the regulator's own channels. An unregistered one has to be approached differently. Registration is not a defence for the firm either way.

It varies with the entity, the evidence, and whether the firm engages early or drags. Some of these ran close to a year. Nobody can give you a date at the start, and anyone who does is guessing.

Yes. The credit card statement is a payment record like any other. In two of these cases the client was actively encouraged to use a credit card to fund further payments, which is worth documenting on its own.

That does not close the matter. Verbal acceptance during a call, especially under pressure, is not a settlement. What counts is whether a formal agreement was signed.