Whether you are about to invest with a SEBI-registered advisor or you already have and something feels off, this is the right page to be on.

SEBI registration sounds reassuring. The advisor has credentials, speaks confidently, and the registration number is right there on their website. For most people, that is enough to feel safe.

But is it actually enough?

The honest answer is: SEBI registration is a starting point, not a safety guarantee. Thousands of registered advisors operate with complete integrity.

But a meaningful number use that registration as a trust signal, a credential that lowers your guard, while quietly violating the very rules they agreed to follow.

This blog will help you understand what SEBI registration actually means, what to check before trusting an advisor with your money, and what steps you can take if you believe a registered advisor has already caused you harm.

SEBI Registration: What It Proves and What It Does Not.

Let’s answer the core question directly.

A SEBI registration confirms one thing: The entity met a set of eligibility criteria at the time of registration. It passed a qualification requirement. It submitted the right documents.

That is all the registration confirms.

It does not prove ethical conduct, nor does it assure honest advice. An advisor may still fail to follow the rules even after receiving registration.

Registration is an entry requirement, not a performance guarantee.

Think of it like a driving licence. Holding one confirms you passed a test on a specific day.

It says nothing about how you drive on every road, every day, after that test. That is why registration should be seen as the starting point of trust, not the final reason to trust.

Is It Safe To Invest With SEBI Registered Advisors or Not?

If you lost money after trusting a SEBI-registered advisor, you’re probably struggling with a question that feels impossible to answer.

How could someone regulated by SEBI leave you with losses, unanswered questions, or a feeling that you were misled?

You trusted the registration. You assumed that if an advisor was approved by the regulator, there would be safeguards in place to protect investors like you. That assumption is completely understandable.

But the reality is that SEBI registration is not a guarantee that every advisor will always follow the rules or act in an investor’s best interest. Registration creates accountability, not immunity from misconduct.

So, is it safe to invest with SEBI-registered advisors?

In many cases, yes, provided you verify them properly before investing. But registration alone is not your protection.

It is a credential that confirms eligibility, not one that guarantees the advisor will always follow the rules or act in your best interest.

The real protection you have as an investor comes from two things: the steps you take before trusting someone with your money, and the complaint mechanism that SEBI registration makes available if something goes wrong.

To understand why both matter, start with what you should actually check before handing over your money.

How to Check If an Advisor is Registered With SEBI?

Before you invest a single rupee, here are the things that actually protect you, not the registration number alone.

- Verify them directly on SEBI’s website: Go to SEBI’s official website and search the registered intermediaries section. Confirm the advisor’s name, registration number, and that their registration is currently active, not expired or cancelled.

- Understand what they are registered as: There is a significant difference between a SEBI-registered Investment Adviser (IA) and a Research Analyst (RA). An IA is authorised to give personalised investment advice based on your financial situation. An RA can only provide general research reports; they cannot legally give you specific buy/sell instructions tied to your capital. Many investors do not know this distinction, and some unregistered or misregistered entities exploit it.

- Ask for a written advisory agreement: A legitimate SEBI-registered Investment Adviser is required to sign a formal agreement with you before providing any advice. If an advisor is hesitant to give you anything in writing, that hesitation is your answer.

- Know the fee rules: SEBI caps the fees that registered Investment Advisers can charge. As of current regulations, fees cannot be linked to profits, and large upfront lump-sum demands are a red flag. If an advisor asks for payment through a personal bank account or in cash, stop.

- Check SEBI SCORES for past complaints: SEBI’s SCORES portal maintains a record of investor complaints against registered entities. A quick search of the advisor’s name or registration number before you invest takes two minutes and could save you significant losses.

From Financial Loss to Full Recovery: Real Arbitration Success Stories

Not every investor dispute ends in silence or loss. While many people assume that once money is gone, it cannot be recovered, real cases show that the outcome can change when facts are properly presented and the right process is followed.

The following cases are examples of investors who faced advisory disputes but chose to take action instead of giving up.

Case 1: Profit Sharing Violation by Aurostar Investment Advisory

“Sir, this is a SEBI-registered company. You don’t need to worry.”

For many investors, that single statement is enough to lower their guard.

One investor did exactly that. He trusted the registration, paid the advisory fees, and followed the recommendations. Why wouldn’t he? A SEBI registration is supposed to signal credibility and compliance.

But over time, things started happening that should never feel normal in an advisory relationship.

The warning signs included:

- The investor’s risk-bearing capacity was only ₹1-3 lakh, yet proper suitability checks were not conducted before advice was provided.

- Despite an agreement that capped annual fees at ₹1.47 lakh, the investor was allegedly asked to pay an additional ₹5 lakh in cash.

- He was reportedly instructed to make the payment through his wife’s account.

- The dispute also involved concerns regarding profit-linked compensation, where the advisor’s earnings became connected to the client’s gains.

- Advice was allegedly being delivered through calls and WhatsApp, despite official documents stating that recommendations would be provided through SMS.

By the time the dispute reached arbitration, the damage had already been done.

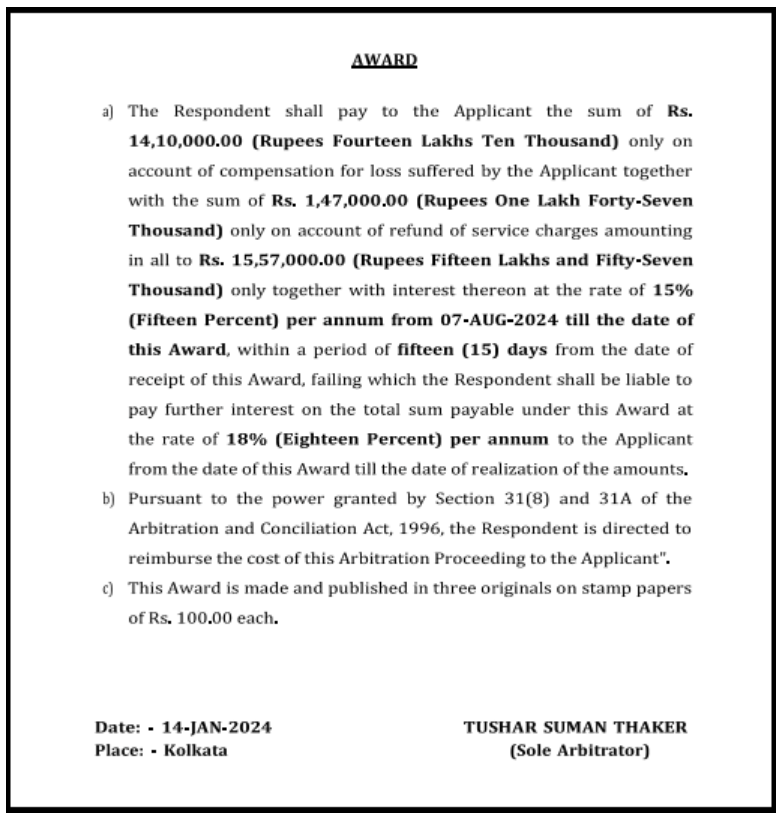

The victim had documented his case properly and presented all the proofs.

The arbitrator eventually awarded ₹14.10 lakh as compensation for losses, ₹1.47 lakh as a refund of service charges, along with interest at 15% per annum.

The most important lesson from this case is not about the compensation amount. It is about the first sentence.

The firm was SEBI-registered. Yet the dispute arose because the allegations involved conduct that appeared to go beyond the rules SEBI had put in place to protect investors.

That is why registration should be seen as the starting point of trust, not the final reason to trust.

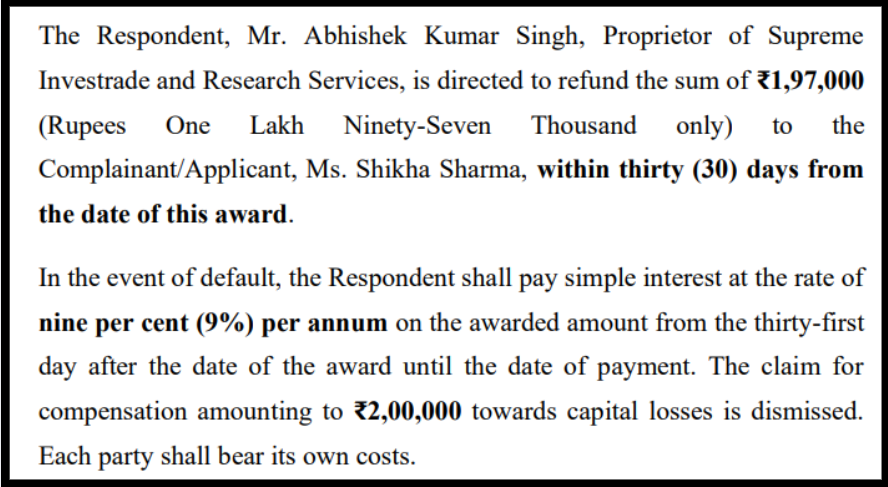

Case 2: ₹1,97,000 Recovery From Supreme Investrade

When Ms. Shikha Sharma signed up for advisory services, she likely believed she was paying for professional guidance that would help her make better investment decisions.

But within less than three months, she had paid ₹1,97,000 to Supreme Investrade and Research Services. Over time, she became concerned that the amount charged to her was significantly higher than the firm’s publicly advertised package pricing.

Like many investors, Shikha was left wondering whether challenging the matter would make any difference.

After registering her case with us, our team carefully reviewed the documents, prepared her claim, and represented her throughout the arbitration proceedings.

The dispute focused on the fees collected by the firm and the representations made during the client relationship.

The outcome was clear.

After examining the evidence, the arbitrator directed Supreme Investrade and Research Services to refund the entire ₹1,97,000 paid by Ms. Shikha Sharma.

For investors who feel that excessive fees have left them with no options, this case shows that the right evidence and the right legal strategy can lead to meaningful recovery.

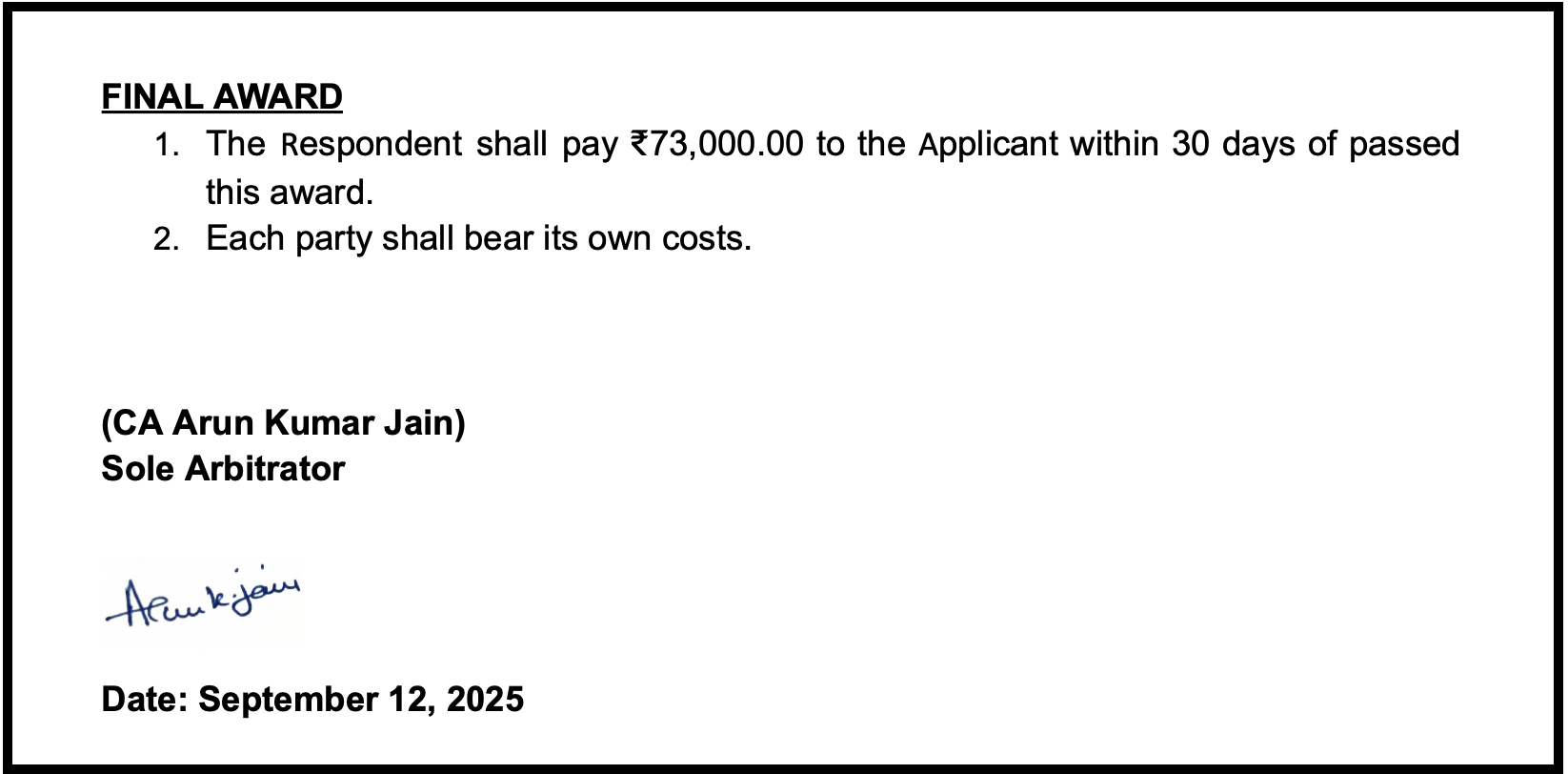

Case 3: ₹73,000 from Falconphase Investment Advisory

When Mr. Naman Sharma signed up for Falconphase Investment Advisory’s “Premium Equity Service,” he believed he was stepping into guided, professional investing. He paid ₹11,900 and expected support, not stress.

At first, everything seemed normal. But soon, he was convinced to share his trading credentials.

That single step changed everything. Without clear consent or control, trades started happening in his account, and within a short time, he had lost ₹73,000.

Like most investors, Naman initially felt there was nothing he could do. The money was gone, and the situation felt final. That is when he reached out for help.

Our team reviewed every detail carefully, including payment proofs, chats, and emails, and then filed his complaint through SEBI’s ODR system.

The matter first went into conciliation, but when that failed, it moved to arbitration.

During hearings, the firm tried to deny responsibility, but key evidence, including their own internal email, worked against them.

On 12 September 2025, Finally, the investor recovered ₹73,000 via SEBI arbitration.

Naman’s recovery proves that financial losses caused by misconduct do not have to be permanent.

If you have faced unauthorized trading or deceptive promises from your advisor, you have the right to fight back.

Take action today and file a formal complaint.

If you want to know the full process first, you can check our full guide on complaint against SEBI registered investment advisor to understand your rights and options.

Advisory Red Flags That Prove Something Is Wrong

It’s easy to trust an advisor when the promises sound convincing, and the early results seem positive. But when something isn’t right, the warning signs usually appear long before the real damage is done.

If any of the following situations sound familiar, it’s worth paying attention because your money could be at risk.

- They showed you profit screenshots from other clients before you paid: Those screenshots are unverifiable. SEBI prohibits advisors from using past client performance as a solicitation tool without specific, mandated disclosures. If a screenshot of someone else’s profits convinced you to pay, the solicitation itself may have been non-compliant.

- The first two calls worked perfectly: This is a known pattern. Early wins build trust and lower resistance to further investment. When the losses start, you are already emotionally committed and financially in. The early wins may have been designed, not predicted.

- Every loss came with a “hold” or “average down” instruction: Legitimate advice accounts for the possibility of loss and has a pre-defined exit strategy. An advisor who responds to every failed call with “add more” and “hold on” is not managing your risk. They are managing their retention of your account.

- Recovery language replaced analysis language: When an advisor shifts from “here is why this trade makes sense” to “losses will recover, trust me”, that shift tells you everything. Analysis is what you paid for. Recovery promises are what they substituted.

- Fees were collected upfront with no refund clause: Legitimate advisors clearly state their fee structure and refund policy. Large upfront fees with blanket non-refundable terms are designed to make walking away expensive after you realise something is wrong.

- You could not get anything in writing: Every significant promise, every trade rationale, every performance claim, your advisor should be able to put it in writing without hesitation. An advisor who avoids documentation is an advisor who knows their promises cannot survive scrutiny.

Need Help?

If a SEBI-registered advisor made you recovery promises that never came through, gave you personalised trade calls that caused losses, collected fees through a personal account, or refused to provide any documentation, your situation has a formal remedy.

We help investors build their case, file through the right channels, and represent them in arbitration proceedings. You do not need to figure out the process alone.

All you need to do is register with us. We will review your situation, guide you on the right recovery path, and get back to you within 24 hours.

Conclusion

A SEBI registration number on someone’s profile is not your safety net. It is a credential that confirms eligibility, not character.

The protection you actually have is the complaint mechanism that registration makes available, and the evidence you preserve from the moment something feels wrong.

WhatsApp chats from the beginning, payment receipts, and screenshots of trade calls often become crucial proof when a complaint is filed.

If something felt wrong with your registered advisor, it probably was wrong. Your next step determines whether that story ends here or ends with your money returning.

File your evidence, build your complaint and take the right step.

Start today because real protection comes from understanding the complaint mechanism and preserving proof the moment something feels wrong.

Frequently Asked Questions

1. My advisor is SEBI-registered but promised me guaranteed returns. Is that still a violation?

Yes, and registration makes it worse, not better.

SEBI explicitly prohibits registered Investment Advisers from promising returns or assuring loss recovery. A registered entity making these promises is violating the regulations they agreed to follow.

That promise, if documented in writing or a recording, is direct evidence for a SEBI SCORES complaint.

2. I paid advisory fees into a personal bank account, not a business account. Can I still get a refund?

The fee collection method itself raises a compliance concern.

Raise it in your formal complaint to the advisor’s compliance officer. Include the payment receipts showing the personal account details.

SEBI takes the traceability of fee collection seriously; it forms part of a broader pattern that strengthens your refund claim.

3. The advisor gave me specific trade calls with entry prices, quantities, and stop losses. Is that allowed under SEBI registration?

A SEBI-registered Investment Adviser is not permitted to provide personalised, specific buy/sell instructions tied to your individual capital and position size.

That scope of activity requires a different regulatory framework.

Specific trade calls, especially when they caused losses, can be cited as a violation in your formal complaint.

4. My advisor says fees are non-refundable and I signed an agreement. Does that mean I have no case?

A contractual non-refundable clause does not override regulatory obligations.

If the advisor violated SEBI regulations through recovery promises, personalised calls, or inadequate disclosures, the fee collection itself becomes challengeable regardless of what the agreement says.

File on SEBI SCORES and let the regulatory process assess the claim.

5. How long does the SEBI SCORES complaint process take for cases against registered advisors?

Initial responses from the registered entity typically arrive within 30 days of filing.

If the response is unsatisfactory, escalating the issue through the SMART ODR complaint portal usually sees movement within 30 to 45 days

Full resolution through adjudication or formal proceedings can take three to six months depending on the complexity of your case and the quality of your documentation.