Most people never see investment fraud coming. It does not arrive as a stranger at the door. It arrives as a trusted friend or a known face.

And by the time you realise what happened, your life savings are gone.

This is the story of one investor who lost ₹2.02 crore, not to a random scammer but to someone her best friend personally vouched for, her best friend’s fiancé.

That relationship is exactly why she never questioned him.

Should You Give Someone Access to Your Trading Account?

Handing over your trading account credentials feels like a small, convenient step. It is not. It is the moment you lose control of your own money.

Consider this: when the person managing your money is your best friend’s fiancé, trust comes automatically. That closeness silences every question you would ask a stranger.

And that assumption is precisely what makes it dangerous.

Once you share your trading platform login, you stop seeing what happens in real time.

You depend entirely on what the other person chooses to tell you. Gradually, you stop questioning. You stop verifying and instead trust the numbers they send you, rather than checking them yourself.

In this case, the victim who reached out to us, Reena (name changed), trusted her best friend’s fiancé, Kshitij Dinesh Joshi, and provided him full access to her trading account, allowing him to handle every trade on her behalf.

He sent weekly profit statements. The numbers looked extraordinary. So she kept investing more. She never logged in to check herself.

By the time she did, the account had ₹5,000 left.

Trust does not protect your money. Only vigilance does. And before we go further, it is important to understand what the law says about this kind of arrangement.

Real Case of an Alleged High-Return Trading Operation

This case followed a pattern seen in many unregistered investment schemes: extraordinary early gains, escalating pressure to add more funds, and total collapse when the truth finally surfaced.

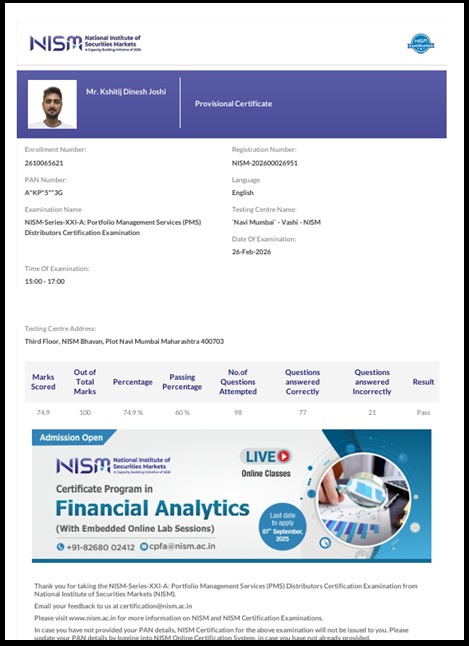

In this case, Kshitij Joshi, who was holding a NISM Provisional Certificate for PMS distribution, reached out to Reena, offering high-return investment schemes.

Reena, trusting Kshitij, invested a huge amount, along with giving him full control of her account. He shared the weekly profit report with her, which gave her assurance, and she kept adding more investment.

Here is how her trust was first built and then broken into pieces, causing not just severe financial losses but also deep emotional distress.

What made Kshitij particularly dangerous was the image he had carefully built around himself.

To everyone in Reena’s circle, he appeared to be a simple, decent man, well-cultured, responsible, with strong family values. Someone nobody would normally suspect.

He used his relationship with his fiancée to gain proximity and emotional trust, and then extended that trust to her closest friend.

But behind this carefully maintained image, he was allegedly operating with calculated intent, using personal relationships as cover to gain access to money and exploit the people who believed in him most.

Phase 1: Trust Built on Big Returns (September–October 2024)

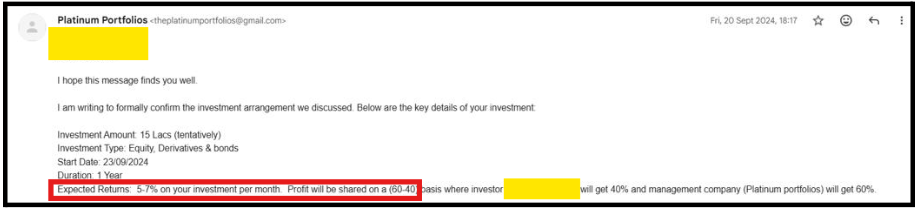

Kshitij proposed managing Reena’s funds through a structure he called “Platinum Portfolios.”

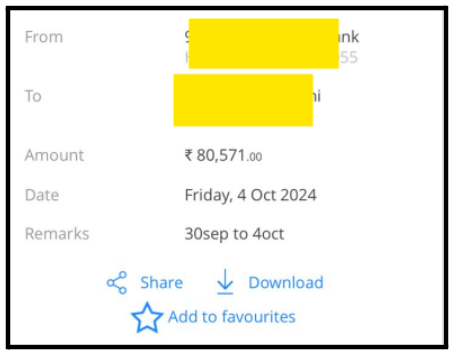

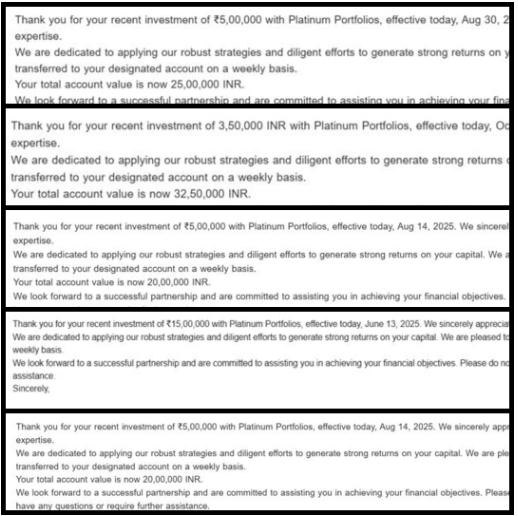

She started with ₹80,571. Within the first week, his associate sent a profit statement reporting ₹2.07 lakh in gains.

The reported portfolio value jumped to ₹17.99 lakh. Reena was thrilled. She added more funds immediately.

Phase 2: Escalating Investments (October–December 2024)

Weekly statements reported profits of ₹3.76 lakh, then ₹7.58 lakh, then ₹10.96 lakh.

The reported portfolio value crossed ₹1.7 crore. Kshitij allegedly celebrated with her. He talked about hitting ₹1 crore in profit by his birthday in March.

Reena invested a total of approximately ₹2.02 crore across the relationship, personal savings and family funds combined.

Phase 3: Losses Blamed on Everything (January–May 2025)

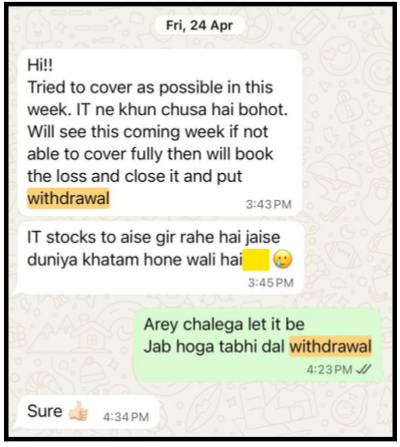

The tone changed. Kshitij blamed the Union Budget. He blamed geopolitical events and reported “no profit” weeks and then actual losses.

He asked Reena for small top-ups to cover “margin shortfalls.” She trusted him and complied each time.

Phase 4: Withdrawal Requests Refused (Mid-2025 to Early 2026)

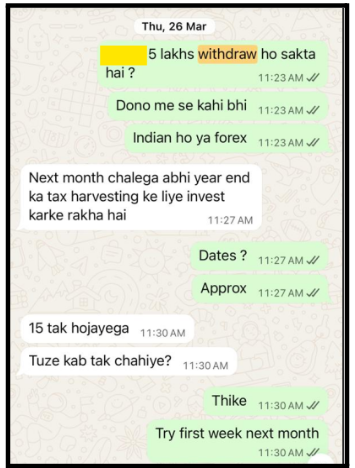

Reena needed ₹5 lakh for personal use. She asked Kshitij to process the withdrawal, and he delayed. He cited “tax harvesting” and said funds were locked in positions.

He allegedly found a new reason every time. She never received the money.

Phase 5: The Collapse, ₹5,000 Left in the Account (May 2026)

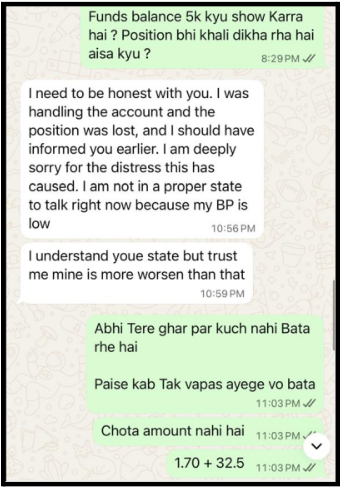

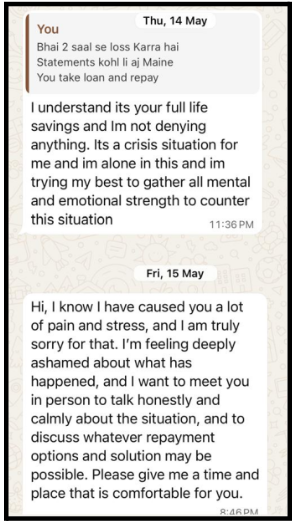

On 14 May 2026, Reena logged into her Zerodha account herself for the first time in months. The funds balance read ₹5,000. No open positions. Nothing.

She confronted Kshitij directly. He admitted the position had been lost. He apologised and said he was not in a proper state to talk.

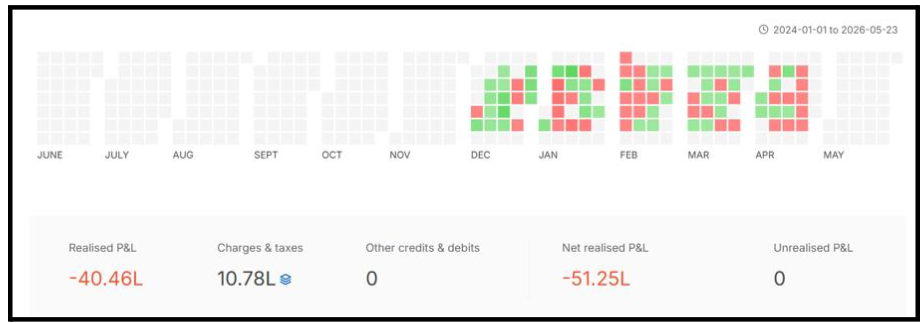

Trading records reviewed by us showed a loss of over ₹51 lakh. F&O records from August 2024 to May 2026 showed cumulative losses exceeding ₹40 lakh.

Bank records confirmed Reena transferred approximately ₹2.02 crore(1.7 crore+32.5 lakhs) to Kshitij over the entire period.

Phase 6: The Confession (May 2026)

Kshitij Joshi acknowledged his failure in writing. He stated he was “standing below zero, not just financial loss but emotional as well as relationship loss.”

He promised repayment. As of the time Reena reached out to us, no repayment had occurred, and no repayment plan existed.

Even when confronted about the losses and the damage caused, Kshitij showed no remorse or accountability. His alleged response, “Put me in jail, you still won’t get your money back”, was deeply disturbing.

Such a statement reflected a complete absence of guilt, empathy, or responsibility toward the people who had trusted him. It raised concerns, in Reena’s view, that this behaviour reflected a pattern rather than an isolated lapse.”

Every stage of this case follows a recognisable pattern. The next section breaks down the lessons that can protect you.

What Can You Learn From This Case?

This case carries lessons that every investor needs to understand, especially when money and relationships are involved.

- Betrayal hides inside trust. Reena did not invest with a stranger. Kshitij was her best friend’s fiancé. That personal connection is exactly what made her lower her guard.

- Manufactured returns create manufactured trust. The early profits were extraordinary. They were also the hook. High, consistent returns in the first weeks of an arrangement are designed to make you invest more.

- You must verify independently. Log into your own account. Check your own P&L. Do not rely only on statements your manager sends via chat or email.

- Protecting yourself starts before you invest. Always confirm SEBI registration before transferring money. Ask for the registration number. Never hand over login credentials or OTPs.

- Once you sense something is wrong, act immediately. Reena postponed checking her account for months. Every month of delay made recovery harder. If your gut says something is off, verify it that day.

These lessons only help if you can also spot the warning signs in time. Here they are.

Investment Fraud Red Flags Every Investor Must Know

What starts with trust and high returns can end in massive financial losses.

Understanding the risks of following unverified stock tips and unregistered investment arrangements is one of the most important steps any retail investor can take before committing money to any advisory setup.

Here are the warning signs every investor should learn before investing:

- Guaranteed or unusually high returns. No legitimate investment promises fixed returns. Anyone guaranteeing 30%, 50%, or higher monthly gains is misrepresenting reality.

- No SEBI registration. A legitimate portfolio manager, investment advisor, or stockbroker holds a verifiable SEBI registration number. Demand it before you invest a single rupee.

- No formal written agreement. Professional investment arrangements involve legal contracts. WhatsApp messages and informal emails offer you no legal protection.

- Constant pressure to add more funds. Fraudulent operators create urgency. They tie up your withdrawals and keep pushing you to top up.

- Difficulty withdrawing your own money. Any delay, deflection, or invented reason why you cannot access your funds is a critical warning sign. A legitimate manager never blocks your withdrawal.

- Requests for account credentials or OTPs. No authorised professional needs your trading login or one-time password. If someone asks for these, they are taking unauthorised control of your account.

- No independent access to your own account activity. If your only record of portfolio performance comes from just your manager’s messages, you have already lost visibility over your money.

Recognising these signs is the first step. Acting on them is what protects you. Here is exactly what to do.

What SEBI Says About Unregistered Portfolio Management Services?

SEBI’s rules are clear and non-negotiable. Anyone managing another person’s money on a discretionary basis must hold a valid Portfolio Manager registration under the SEBI (Portfolio Managers) Regulations, 2020.

An unregistered operator cannot legally trade on your behalf. They cannot exercise control over your account without your approval for every transaction. They cannot promise fixed or guaranteed returns of any kind.

Kshitij Joshi held a NISM Provisional Certificate for PMS Distributors.

That certificate only allows someone to sell or distribute PMS products of already-registered entities. It does not authorise him to run his own portfolio management operation or take discretionary control of anyone’s account.

He allegedly did both. And Reena trusted him for nearly two years.

Knowing SEBI’s rules could have stopped this early. Now, let us look at exactly how it unfolded.

How to Complain Against Platinum Portfolios?

If you suspect you are a victim, every hour matters. Unregistered advisors and operators leave financial trails, but those trails get harder to follow with time.

Here is how to respond:

Step 1: Secure All Your Evidence

Download every chat, every transaction screenshot, every bank statement, every email, and every profit statement right now. Save them in multiple locations.

Do not tip off the accused before you have everything. This evidence is the foundation of every legal action that follows; without it, your case is significantly weaker.

Step 2: Contact the Entity Directly and Document Every Response

Send a formal written email or message to the individual, company, or advisory entity involved. Clearly ask for explanations, account statements, pending funds, and transaction details.

Keep records of every reply, delay, excuse, or refusal, as these communications may later become important evidence.

Step 3: File a Complaint with SEBI

Send a detailed written complaint to SEBI against the unregistered operator, in this case an entity like Platinum Portfolio, explaining the complete sequence of events.

Attach all supporting evidence, including statements, screenshots, transaction proofs, and communication records.

A written complaint creates an official regulatory trail and may help initiate further examination of the matter.

Step 4: File a Cyber Crime Complaint

If online fund transfers, trading platform misuse, or unauthorised account access are involved, file a cybercrime complaint without delay.

Provide complete evidence, including bank transfer records, Telegram chats, emails, trading statements, screenshots, phone numbers, UPI IDs, and account details linked to the individual or entity involved.

Step 5: Consult a Legal Expert

For larger losses, speaking to a lawyer who handles securities matters can help you understand your options for civil recovery.

The faster you act, the stronger your chances of protecting your financial interests and preserving critical evidence. Delays often make recovery, investigation, and legal action far more difficult.

Need Help?

We work with investors across India who have suffered losses through unauthorised trading setups, unregistered portfolio management arrangements, and high-risk investment schemes.

- Case Review: We review chats, bank transfers, trading statements, and other records to identify the strongest evidence supporting your case.

- SEBI and Regulatory Complaint Assistance: We help prepare structured complaints for the SEBI and relevant authorities, ensuring your evidence is properly organised.

- Documentation and Timeline Preparation: We help organise transactions, conversations, and financial records into a clear timeline that supports legal and regulatory action.

If you believe you may be facing a similar situation, register with us. The sooner evidence is secured and documented, the stronger your position becomes.

The facts presented in this article are based on information and evidence provided by the complainant. This is not a court verdict or legal finding. The named individual has not been adjudicated guilty by any court of law.

This article is published in the public interest to raise awareness about unregistered investment schemes and to assist the complainant in reporting the matter to the relevant regulatory authorities.

Conclusion

Investment fraud in India thrives on trust. It targets the people who believe in someone, not random strangers. It uses manufactured returns to keep doubt silent.

And when it finally collapses, it leaves victims with nothing but a mountain of evidence and nowhere to start.

Reena lost ₹2.02 crore. She lost two years of hope. She came to us, and we stood beside her.

You can protect yourself. Verify SEBI registrations. Never surrender account access. Check your own statements every single week. Withdraw early if something feels wrong.

And if you are already in this situation, act now. Secure your evidence. You deserve to recover what is yours.