Is a SEBI-registered investment advisor safe or not? It is the single most important question you should ask before trusting anyone with your money.

Thousands of investors across India assume that a SEBI registration certificate equals complete safety. That assumption, unfortunately, costs many of them dearly.

Let’s dive into every perspective related to it through this blog.

SEBI Guidelines for Investment Advisors

A SEBI-registered investment advisor (IA) is an individual or entity holding a valid certificate of registration under the SEBI (Investment Advisers) Regulations, 2013.

An IA charges fees to provide personalised investment advice to clients on securities, financial products, and portfolio strategies.

Crucially, an IA must act in a fiduciary capacity, meaning the client’s interest must always come first, above the adviser’s own financial gain.

You always need to check what a SEBI-registered IA can do and what it can not to understand the guidelines properly.

| What an IA Can Do | What an IA Cannot Do |

| Provide personalised investment advice on securities and financial products | IA cannot execute trades on behalf of clients |

| Charge a flat fee or AUM-based fee within SEBI’s prescribed limits | Charge commissions, referral fees, or profit-sharing arrangements |

| Offer risk profiling and financial planning services | Guarantee returns or promise assured profits of any kind |

| Maintain client records and suitability assessments | Share advice through personal WhatsApp, Telegram, or social media without compliance |

| Provide advice on mutual funds, equities, derivatives, and bonds | Simultaneously act as a broker, sub-broker, or distributor for the same client |

| Operate after obtaining NISM Series-X-A and X-B certifications | Collect or handle client funds directly |

So the next time someone calls themselves a SEBI-registered investment advisor, remember that this title comes with specific permissions and hard boundaries.

An adviser who crosses those boundaries does not become less dangerous because they hold a certificate. In fact, the registration makes their misconduct more calculated and more difficult to detect early.

Is a SEBI-registered Investment Advisor Safe or Not?

A SEBI-registered investment advisor’s safety label gives you regulatory recourse, but it does not eliminate the risk of fraud, poor advice, or financial misconduct.

Registration means the adviser meets entry-level requirements; it does not guarantee that they will act ethically, competently, or in your interest at every moment.

1. Registration Confirms Compliance at Entry, Not Ongoing Conduct

Every IA clears a minimum eligibility bar to obtain SEBI registration: educational qualification, NISM certification, net worth requirements, and a fit and proper declaration.

However, once registered, ongoing compliance depends entirely on the adviser’s own integrity and internal controls.

Consequently, a registered IA can still churn your portfolio, push unsuitable products, or promise guaranteed returns years after receiving that registration.

2. Recovery of Money is Not Guaranteed Even After Proven Fraud

This is the hardest truth about the question of whether a SEBI-registered investment advisor is safe or not.

Even when SEBI proves violations, imposes penalties, and orders refunds, actual recovery of investor money depends on the adviser’s financial position, willingness to comply, and asset availability.

Several SEBI orders against IAs have directed refunds that investors never fully received because the entity dissolved, assets were liquidated, or the directors simply did not cooperate.

3. Conflict of Interest Remains a Persistent Risk

Many investment advisers maintain undisclosed relationships with brokers, mutual fund distributors, or product manufacturers.

These relationships create financial incentives to recommend products that benefit the adviser, not the investor.

SEBI’s regulations prohibit this, but detecting it requires active investor vigilance rather than passive trust in a registration number.

4. Grievance Redressal Takes Time and Documentation

When a registered IA wrongs you, the path to justice runs through SCORES, SMART ODR, and potentially arbitration or court.

Each step demands thorough documentation, time, and persistence. Investors who lack records of payments, agreements, or communications often find themselves unable to prove misconduct even when it clearly occurred.

Does SEBI Take Action Against Investment Advisors?

Yes, SEBI actively monitors registered investment advisers and takes action when it finds violations.

Moreover, it receives thousands of complaints through SCORES each year and also conducts suo motu checks on websites, social media, and advertisements.

When it detects misconduct, SEBI issues a Show Cause Notice, conducts hearings, and then imposes penalties, refunds, or suspensions.

However, it can also pass immediate interim orders when investor harm requires urgent action.

Common Violations By Investment Advisors

SEBI typically takes action against an IA when it finds the following common violations:

- Promising assured, guaranteed, or unrealistic returns to investors

- Operating as an unregistered portfolio manager while holding only an IA licence

- Mixing advisory and execution services through a connected broker

- Collecting client funds directly instead of directing payments to service providers

- Sharing investment tips through personal WhatsApp, Telegram, or social media channels

- Failing to maintain suitability assessments or client risk profiling records

- Charging fees beyond SEBI’s prescribed annual ceiling per client

- Misrepresenting qualifications, track records, or SEBI registration scope

These patterns repeat across most enforcement cases, so spotting even one early can help you avoid significant financial loss.

How Does SEBI Take Action Against IAs?

SEBI follows a structured enforcement process from investigation to final penalty across multiple stages.

- Show Cause Notice (SCN): SEBI outlines charges, violations, and evidence, allowing the IA to respond in writing.

- Interim Ex-Parte Order: SEBI issues an immediate market ban to prevent investor harm, without waiting for a hearing.

- Personal Hearing: SEBI allows the IA to appear, present a defence, and respond to charges.

- Final Order: SEBI reviews evidence and imposes penalties, refunds, bans, or registration actions.

- Referral to Other Agencies: SEBI sends serious fraud cases to agencies like the ED or police for further action.

Importantly, failing to appear for hearings does not protect a noticee. SEBI consistently proceeds on available evidence when an IA refuses to participate in the process.

SEBI Orders Against Investment Advisors

Across India, enforcement actions target registered investment advisers for violations like guaranteed returns and unregistered portfolio management.

The following cases represent some of the most significant recent actions.

| IA Entity | Key Violation | Penalty |

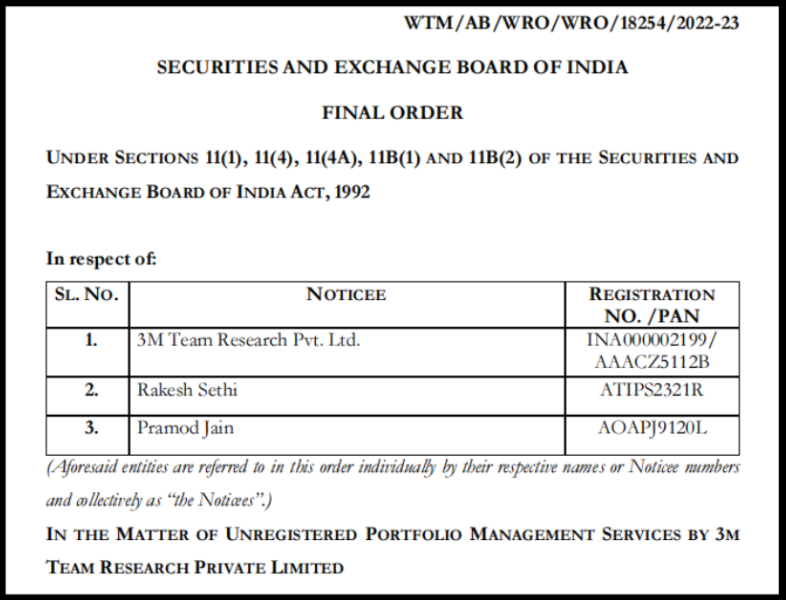

| 3M Team Research Pvt. Ltd.

|

Ran an unregistered PMS, promised 200-400% annual returns, mixed advisory with broker execution | ₹10 lakh + refund of ₹89.4 lakh + 1-year debarment + registration suspended 1 year |

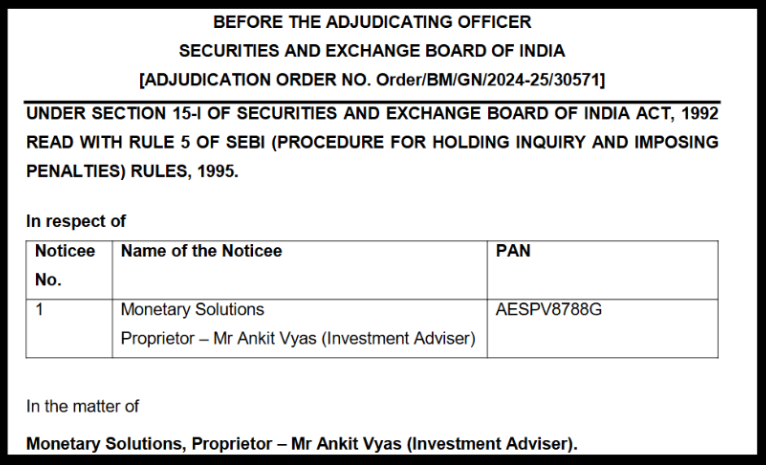

| Monetary Solutions, Prop. Ankit Vyas

|

Fake testimonials on the website, fees collected in a personal account, no client agreements, 7 unqualified staff | ₹25 lakh (July 2024) |

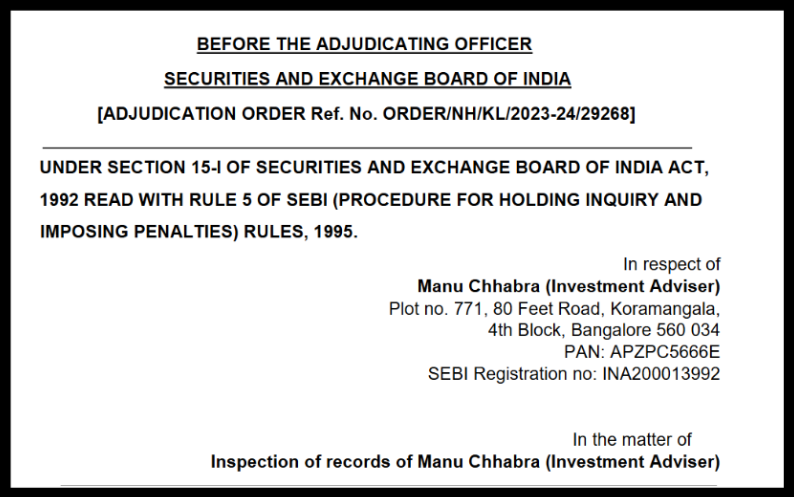

| Manu Chhabra

|

Charged ₹5.16 lakh from one client in a single month, failed to maintain PAN details for 107 of 157 clients | ₹4 lakh (September 2023) |

SEBI’s enforcement record makes clear that registration does not shield an adviser from accountability.

Furthermore, the pattern across all these cases reveals the same playbook: assured returns, fund collection, mixed roles, which means investors who spot any one of these warning signs must treat it as a signal to stop, verify, and escalate.

Impact on Investors

When SEBI acts against a registered IA, investors often find themselves in a difficult position, they have already paid fees, suffered losses, and must now navigate a lengthy recovery process while the IA contests the order.

- Many investors lose the full fee amount even when SEBI orders a refund, because the IA has already dissipated the funds

- Investors who paid through informal channels like personal UPI or cash find it harder to prove payment in formal proceedings

- Those who acted on guaranteed return promises often carry additional market losses beyond the advisory fees

- Delayed complaint filing weakens evidence, as messages, emails, and call records become harder to retrieve over time

The core lesson is this: acting early, documenting everything, and filing complaints at the first sign of misconduct significantly improves recovery outcomes.

How to Check a SEBI Registered Investment Advisor?

Many investors search online for answers like Can I trust SEBI registered investment advisor firms before paying fees?

In most cases, trust should begin with verifying the advisor’s registration number, checking whether the registration is active, and confirming that the services offered match SEBI regulations.

Verifying whether SEBI registered IA is safe or not requires more than a quick registration check.

Start by confirming the adviser’s registration number directly on the official SEBI website under the registered intermediaries section, not through the adviser’s own website or marketing brochure.

- Check that the registration is active and not suspended or cancelled. SEBI updates its records when it imposes enforcement actions

- Confirm the adviser holds valid NISM Series-X-A and X-B certifications. Expired certifications are a compliance violation in themselves

- Verify that the adviser’s name and entity match exactly. Fraudsters sometimes use registration numbers of legitimate IAs to appear credible

After verification, always insist on a written advisory agreement before paying any fee.

The agreement must clearly state the scope of advice, fee amount, duration, and refund terms, and you must sign it before any money changes hands.

Whether a SEBI-registered investment advisor is safe or not ultimately comes down to your own vigilance. SEBI builds the regulatory fence, but you decide whether to look before you step through the gate.

How To Report an RIA in India?

If a registered or unregistered investment adviser has misled you, collected money illegally, or caused financial harm through deceptive practices, India’s regulatory system gives you a structured path to fight back.

Move quickly; the sooner you act, the stronger your case.

Step 1: Document Everything Before You File

Before contacting any authority, gather every piece of evidence you hold: payment receipts, advisory agreements, WhatsApp messages, emails, call recordings, account statements, and screenshots of website claims.

Organise this material chronologically, because every escalation step relies on this documentation as its foundation.

Without records, even the strongest verbal complaint carries little weight.

Step 2: File a Formal Complaint with the Adviser

Send a written complaint to the adviser’s designated grievance officer, clearly stating the nature of misconduct, specific violations, dates, and amounts.

Give the adviser 21 days to respond. If the response is unsatisfactory or absent, that silence itself strengthens your case for escalation and demonstrates that internal redressal failed.

Step 3: File a Complaint in SCORES

File your complaint on the SEBI SCORES platform, which compels the registered IA to respond under SEBI’s direct monitoring.

SEBI assigns a complaint ID, tracks the timeline, and intervenes when the adviser fails to engage.

Many investors resolve disputes at this stage, particularly when the adviser understands that SEBI now watches every step of their response.

Step 4: Register a Complaint with SMART ODR

If SCORES does not deliver a satisfactory outcome, escalate to SMART ODR, SEBI’s Online Dispute Resolution platform which provides structured conciliation and arbitration between investors and registered intermediaries.

SEBI mandates participation from all registered entities, and the conciliation process often produces faster settlements than formal arbitration proceedings.

Step 5: Stock Market Arbitration

If all prior steps fail, file for formal arbitration where an independent panel reviews your evidence and delivers a legally binding award.

An arbitration award carries the force of a court decree. The adviser must comply or face direct regulatory and legal consequences that SEBI and the relevant exchange enforce.

Need Help?

If you have suffered losses or paid fees to a registered or unregistered investment adviser who misled you, our team steps in at any stage of the process and fights for your recovery.

- We review your case in full and identify every SEBI regulation the adviser violated

- We build your complete documentation file, organising evidence, timelines, and legal grounds

- We draft formal complaint letters to the adviser, SEBI SCORES, and the relevant regulatory bodies

- We guide you through SMART ODR conciliation and formal arbitration proceedings from start to finish

Fraudsters count on investor silence and confusion. We turn both into clarity and action. Register with us.

Conclusion

Whether a SEBI-registered investment advisor is safe or not depends on two things: the adviser’s own conduct and your own vigilance.

SEBI’s regulatory framework is strong, its enforcement record is growing, and its investor protection tools are accessible.

However, no registration eliminates the need for personal due diligence.

Verify registrations independently, demand written agreements, reject guaranteed return promises, and document every interaction from day one.

The answer to “Is a SEBI-registered investment advisor safe or not?” is never simply yes or no; it is always: verify first, then decide.