Quick Summary

A SEBI registered Research Analyst publishes the same research and recommendations to every subscriber at once, while an Investment Advisor builds personalised advice on your goals and risk profile, and the registration number tells you which one you are dealing with: INH means Research Analyst, INA means Investment Advisor. The two operate under different regulations, carry a fee ceiling of ₹1,51,000 per family under the fixed fee route, and answer to different complaint desks, where picking the wrong category on SCORES costs weeks. This page covers the differences, what each can and cannot do, and exactly how to complain against either one.

You receive a call from a market expert claiming to have the next big stock opportunity. Another professional offers a complete financial plan tailored to your goals.

Both mention SEBI registration, but one is a Research Analyst and the other is an Investment Advisor, and at this point most investors ask the same question: what is the difference, and which one should I trust?

The distinction matters twice. Once before you pay, because choosing the wrong service leads to unsuitable recommendations and broken expectations.

And once again if things go wrong, because the two categories answer to different rules and different complaint desks, and even the SCORES form makes you choose between them.

This guide covers both moments: the key differences, the regulations governing each, and the complaint route that works when either one fails you.

SEBI Registered Research Analyst vs Investment Advisor India

For a first-time investor, both services may appear similar.

Both discuss stocks, and both provide market-related insights. Both may hold SEBI registration and may charge fees for their services.

However, the similarities largely end there.

A Research Analyst and an Investment Advisor operate under different regulatory frameworks, have different responsibilities, and serve different investor needs.

Think of it this way.

A Research Analyst may say: “Based on our analysis, Stock XYZ appears attractive.”

An Investment Advisor may say: “Based on your age, risk appetite, retirement goals, current investments, and financial position, Stock XYZ may or may not be suitable for you.”

That difference is significant. One provides research-based recommendations. The other provides personalised financial advice.

The table below splits the two across nine dimensions, from who regulates them to how each charges you.

Run through it once before paying either one:

| Basis | SEBI Registered Investment Advisor (RIA) | SEBI Registered Research Analyst (RA) |

|---|---|---|

| Primary role | Personalised investment advice built on your financial situation, goals, and risk profile | Research reports, stock recommendations, and market analysis for a broader audience |

| Regulator | The Investment Advisers Regulations, 2013 | The Research Analysts Regulations, 2014 |

| Nature of advice | Personalised and client-specific | General research-based recommendations |

| Risk profiling | Mandatory before any advice | Generally not required, since nothing is tailored |

| Financial planning | Full planning, retirement, goals, and asset allocation | Cannot provide personalised planning |

| Suitability duty | Must ensure advice suits your profile and objectives | Focuses on analysis, not individual suitability |

| Products covered | Mutual funds, stocks, bonds, insurance-linked products, and portfolio strategy | Stocks, derivatives, commodities, sectors, and indices in research reports |

| Managing your money | Cannot manage funds unless separately authorised | Cannot manage funds or execute trades at all |

| How they charge | Advisory fees within SEBI’s limits | Subscription fees for research services |

How Do You Know If You Are Dealing With a SEBI Registered Research Analyst or Investment Advisor?

Before the bigger differences, here is the two-minute check that settles the question for any firm in front of you, and it matters both before you pay and when you complain.

1. Check the Registration Number First, Because it is Definitive

An INH prefix means Research Analyst, so INH000012345 is a Research Analyst registration.

An INA prefix means Investment Advisor, so INA000067890 is an Investment Advisor registration.

Search the firm’s name on SEBI’s registered intermediaries portal, and the category beside the number confirms it.

2. Then Check What You Actually Received

The firm that sent the same Nifty options call to 5,000 subscribers on WhatsApp at 9:17 AM is a Research Analyst, because everyone got the same call at the same time.

The firm that assessed your goals, risk appetite, and tax situation before recommending anything is an Investment Advisor, because the advice was built for you alone.

And if no registration number appears anywhere, on the website, the agreement, or the marketing, that itself is a compliance gap, and the firm may be unregistered, which changes everything about your route if money is involved.

Is a Research Analyst Allowed to Give You Personalised Tips?

This is one of the most misunderstood areas in the securities market.

Many investors assume that SEBI registered research analysts can provide stock recommendations tailored to their income, financial goals, risk appetite, investment horizon, and personal circumstances.

A Research Analyst provides research-based recommendations, market analysis, stock reports, and investment ideas.

However, personalised financial advice tailored to an individual’s income, assets, liabilities, risk tolerance, and financial goals is the role of an Investment Advisor.

This is why investors should clearly understand what a SEBI registered RA can do before subscribing to any service.

A Research Analyst can publish and communicate research recommendations, but you should never assume a recommendation is personalised to your specific financial circumstances.

The full answer, with what crosses the line, is in our guide: Can research analyst give personalized tips in India?

Should a SEBI Research Analyst Recommendation Come Without a Stop Loss?

Technically, no regulation forces every recommendation to carry a stop loss, which surprises most investors who assume it is mandatory.

Yet many analysts include one anyway, and the reason connects to what the rules actually demand: fair disclosure of risk, not just targets.

So when a recommendation shows you only the profit side, something is missing, and knowing what a complete recommendation should contain protects you before the trade, not after.

What the regulations actually require, and when a missing stop loss becomes a genuine complaint ground, is covered in our guide on whether a SEBI research analyst can give trades without stop loss.

Can Research Analysts Recommend Your Exact Lot Size?

Imagine a message that says buy 5 lots of this option immediately. Confident, specific, and for many investors, completely convincing.

Here is the catch: an exact lot size can cross the line from research into personalised advice, because how much you should trade depends on your capital and your capacity for loss, which a Research Analyst is not assessing.

A position right for one trader can sink another, which is exactly why the line exists.

Where the regulatory line sits, and what a message like that one tells you about the firm sending it, is in our guide on whether research analysts can recommend exact lot sizes.

What Exactly Is a SEBI Registered Investment Advisor Allowed to Do?

This is where the role becomes substantially different, because a SEBI registered IA must understand you before advising you.

Picture two investors, a 25-year-old chasing aggressive growth and a 60-year-old protecting a retirement corpus. A Research Analyst may send both the same report. An Investment Advisor would advise them differently, because the advice must fit the person.

That suitability duty, built on your goals, risk tolerance, income, and horizon, is the heart of the role, and it changes what you can expect and what you can complain about.

The complete scope, from what the assessment involves to what an advisor cannot do, sits in our guide on what a SEBI registered investment advisor can do in India.

What Is the SEBI Fee Limit for RA and IA?

To protect investors from excessive charges, SEBI caps what both categories can collect, and the current limits matter because plenty of older pages still quote the outdated ones.

The ceiling now works like this, and note where the two categories differ:

| Fee Basis | SEBI Permitted Limit |

|---|---|

| Fixed fee, for both RA and IA | Up to ₹1,51,000 per family per annum |

| Assets under advice based fee, IA only | Up to 2.5% of AUA per annum |

| Profit-linked or profit-sharing fee | Not permitted for either |

Two details most investors never learn.

The caps run independently across the two categories.

A subscription with a Research Analyst and another with an Investment Advisor in the same year are each measured against their own ceiling, so holding both creates no combined limit issue.

And GST sits on top, because the cap applies to the base fee, not the tax.

Before engaging either one, ask for a written fee structure and check it against these limits, because fees demanded beyond the ceiling, or any profit-sharing proposal, is a regulatory compliance issue in itself.

Is a Refund Possible from a SEBI Registered Research Analyst?

This is one of the most searched questions from investors who paid membership fees and then experienced poor performance, non-responsiveness, or service disputes.

The answer is nuanced, and SEBI registration itself does not create an automatic refund entitlement.

A refund typically depends on the service agreement, the representations made, the evidence available, and the facts of the dispute. Requests usually arise from misrepresentation of services, services not delivered as promised, unauthorised charges, or communication breakdowns.

It is worth noting that SEBI does not itself adjudicate refund claims.

It investigates regulatory violations and can act against the registered entity, while your refund claim is most effectively pursued through the ODR platform or consumer courts, with the SCORES complaint pursuing the regulatory angle simultaneously.

The full picture, including the pro rata refund rule for advance fees, sits in our guide: Can I get refund from SEBI registered research analyst?

SEBI vs Eqwires: What the Order Covers?

One of the most important lessons for investors is that SEBI registration category matters just as much as the SEBI registration itself.

A person registered as a Research Analyst (RA) cannot automatically perform activities that fall within the scope of an Investment Adviser (IA).

This distinction became a major issue in the SEBI order against Eqwires research analyst, where the entity’s regulatory boundaries were examined

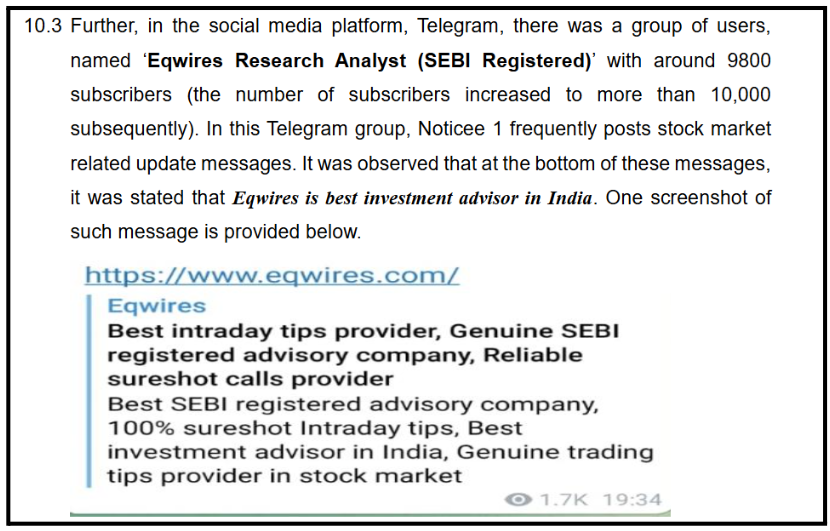

Eqwires was alleged to have held itself out as an investment adviser through its website, social media channels, Telegram groups, and promotional content despite not holding an Investment Adviser registration.

SEBI observed that the entity used phrases such as “best investment adviser” and “stock advisory company,” which created the impression that it was providing investment advisory services rather than research analyst services.

The regulator also noted concerns relating to the nature of services being offered, including activities that appeared to go beyond the scope of research analysis.

SEBI further observed issues relating to misleading promotional claims, testimonials, and representations made to investors.

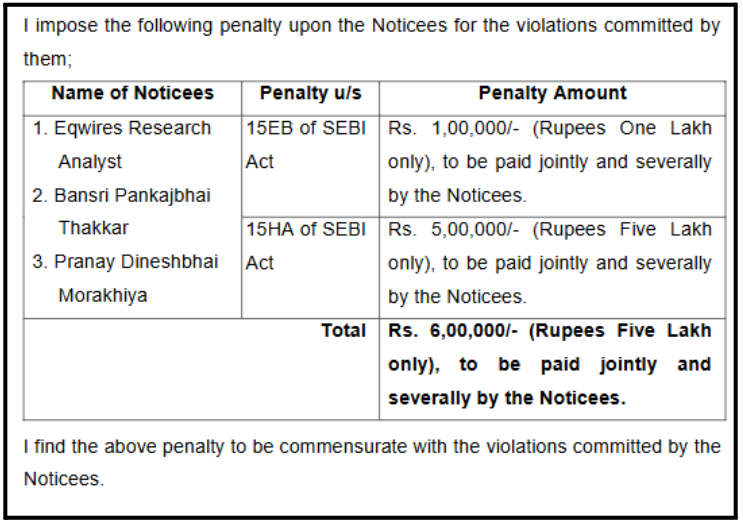

Following the proceedings, SEBI imposed a total penalty of ₹6 lakh on Eqwires Research Analyst and its partners.

The penalty consisted of:

- ₹1 lakh for violations relating to Research Analyst and Investment Adviser regulations.

- ₹5 lakh for fraudulent and unfair trade practice-related violations.

The Eqwires matter highlights an important principle for investors.

Before subscribing to any service, do not simply verify whether the entity is SEBI registered. Also, verify what type of registration the entity holds.

A Research Analyst can provide research reports, market analysis, and recommendations.

An Investment Adviser, on the other hand, is authorised to provide personalised investment advice after considering an investor’s financial circumstances and suitability requirements.

Understanding this distinction can help investors better evaluate the services being offered and identify situations where promotional claims may not match the registration category under which the entity operates.

If you find yourself in a situation where a registered entity has misrepresented its registration category, such as an RA giving personalized advice or managing your portfolio, you have the right to seek redressal.

When seeking refunds or taking action against such entities, you can pursue your case through consumer courts or the ODR platform.

For a detailed, step-by-step walkthrough on how to initiate this legal and regulatory process, you can follow this comprehensive guide on how to file a complaint against RIA to navigate the system effectively and protect your capital

Need Help Resolving a Dispute?

Don’t navigate complex regulatory steps and messy paperwork alone.

Reach out to us today so we can evaluate your case, organize your documentation, and guide you through the right grievance redressal path.

How to Complain Against a SEBI Registered Entity?

Whether you have been wronged by an RA, an RIA, or any other registered intermediary, the complaint process is structured, free to begin, and needs no lawyer.

Acting quickly and preserving your evidence is the single most important thing you can do, because every stage that follows stands on the record you keep from day one.

The road itself is the same one every investor dispute travels.

It starts with your evidence and a written complaint to the firm itself, whose reply or silence becomes the foundation of the case.

When that answer disappoints, a SEBI SCORES complaint puts the regulator’s record behind the dispute, and the firm’s obligation to respond there is regulatory, not optional.

Beyond the regulator sits free conciliation through the online dispute resolution system, and for the cases that refuse to settle, the final stage of arbitration in share market proceedings delivers a binding decision.

Every stage, portal, and timeline on that road is covered on the guides linked above.

What this page adds is the one choice on that road that belongs to this topic alone, the selection that decides which desk your complaint reaches.

Which Category Do You File Under on SCORES?

Here is the selection inside step 3 that decides how fast everything moves, and it is the single most common filing mistake investors make.

The SCORES form asks you to pick an intermediary type, and picking the wrong one routes your complaint to the wrong desk inside SEBI’s system, where it gets returned for correction or redirected, adding weeks before anyone reads the actual grievance.

The rule is the one from the identification check above: Research Analyst with the INH number, or Investment Advisor with the INA number, and the prefix never blurs.

The desk is not the only thing that changes. The rulebook changes with it.

For Research Analysts, the commonly violated rules are guaranteed return claims, personalised execution calls, account handling, and fees collected in personal accounts.

For Investment Advisors, the framework runs on risk profiling before advice, a written agreement before fees, and no profit sharing. The same conduct described under the wrong framework can read as no violation at all.

When one firm holds both registrations, and some do, the category follows the service, not the firm.

A complaint about their recommendation newsletter files under the INH number, and a complaint about their personalised advisory files under the INA number, with the service agreement you signed naming which registration your subscription sat under.

Match your situation to the rows below, and the second column is your answer:

| Your Situation | File Under |

|---|---|

| Paid for intraday or index option tips sent to all subscribers | Research Analyst, with the INH number |

| Subscribed to a stock picks or multibagger recommendation service | Research Analyst, with the INH number |

| Paid for a personalised advisory built on your goals and risk profile | Investment Advisor, with the INA number |

| Received the same market commentary as every other client | Research Analyst, with the INH number |

| Paid for an algo or automated calls subscription | Usually Research Analyst, but check the prefix first |

How to Verify Whether an Entity Is SEBI Registered?

Before paying any subscription fee, advisory charge, or investment-related fee, investors should independently verify whether the entity is genuinely registered with SEBI and authorised to provide the services being offered.

Many investors rely solely on advertisements, social media promotions, WhatsApp messages, or verbal assurances from sales representatives, but these sources should never be treated as proof of regulatory registration.

The safest approach is to verify SEBI registration number directly through official SEBI records.

Investors should carefully check the registration number, registration category, and validity of the SEBI registered research analyst license.

Checking the official contact details and the name of the individual or organisation listed in SEBI’s database ensures you aren’t dealing with an expired or suspended entity.

It is also important to confirm whether the registration category matches the services being offered.

For example, a SEBI-registered Research Analyst is permitted to provide research recommendations, while a SEBI-registered Investment Advisor may provide personalised investment advice subject to regulatory requirements.

Therefore, registration verification should be viewed as the first step of due diligence rather than the final decision-making factor before making a payment.

Conclusion

A SEBI registered research analyst, with the INH prefix, publishes general research and recommendations, and is not authorised to give advice tailored to your individual situation.

A SEBI registered investment advisor, with the INA prefix, provides personalised, suitability-assessed advice, within SEBI’s fee and conflict rules.

Both operate under separate frameworks, serve different needs, and a complaint against each lands at a different desk; registration authorises them to operate without guaranteeing profits, eliminating risk, or automatically entitling you to refunds.

Before subscribing, verify the registration and its category, understand the service, and preserve every record.

And if it ever comes to a complaint, the prefix that identified the firm is the same one that routes your filing to the right desk the first time.

Report. Recover. Stay Fraud Free.

Frequently Asked Questions

No. Research Analysts focus on research and recommendations published to subscribers generally, while personalised financial planning built on an individual's situation belongs to the Investment Advisory category under a separate set of SEBI regulations.

Under the fixed fee mode, up to ₹1,51,000 per family per annum, or alternatively up to 2.5 percent of assets under advice per year. The advisor must stick to one model for a client, and profit linked fees are not permitted in either mode.

The registration prefix decides it, with INH meaning Research Analyst and INA meaning Investment Advisor. If the firm holds both, the category follows the specific service your complaint concerns, and the service agreement names which registration your subscription sat under.

An RA can distribute financial products with full conflict of interest disclosures. An RIA cannot distribute products and advise the same client simultaneously, since SEBI mandates strict separation so advisors never recommend products they earn commissions on.

Bad advice alone does not create a refund right, since market risk is inherent. But regulatory violations, like fees in unauthorised accounts, fraudulent guarantees, or services never delivered, open refund claims through the ODR platform or consumer courts, with SCORES carrying the regulatory angle in parallel.